Roland Berger advises Pharma, Life Science and MedTech companies on how to master the challenges of the future.

Trump tariffs reshape global trade flows

By David Born

US imports from China plunge while Mexico and Southeast Asia gain ground

Since President Trump’s inauguration in January, US import tariffs have come under increased scrutiny. We took a closer look at the 2025 trade data to address a pressing question: are global trade flows already shifting? In this update, we examine Canada, Mexico, and China; the initial countries subjected to new tariffs in early 2025 as well as secondary effects, notably the rerouting of trade through Southeast Asian economies.

Hours after being sworn in, Trump imposed 25% tariffs on Canada and Mexico starting February 1, accusing both countries of allowing drugs and migrants to cross the US border. Just days after taking effect, the tariffs were paused for 30 days following threats of retaliatory measures - shifting the final effective date to March 4. Given the trade agreement between the three partners (USMCA), a bulk of imports remain duty-free, with the 25% rate applying only to non-exempt goods.

Recent data indicate significant shifts in US import patterns. US imports from Canada fell from $38 billion in January to $30 billion in May; a steep drop that, according to the US Energy Information Administration, was largely due to a decrease in energy imports, particularly crude oil.

In contrast, US imports from Mexico peaked at nearly $48 billion in March, supported by regional integration and logistical advantages – factors highlighted by IMF and OECD analyses. Tariff-driven supply chain shifts provided another boost, as US buyers replaced some Chinese imports with USMCA-compliant goods from Mexican factories.

While the immediate impact on Mexican and Canadian imports is noteworthy, the most striking development lies in the steady drop in US imports from China. US imports from China halved between January and May 2025. After the Trump administration announced a 10% tariff rate on Chinese goods in February and an additional 10% in March, the Chinese government retaliated with tariffs on US farm products. The tariff cycle peaked at 145% for Chinese goods before Washington cut the baseline tariff rate to 30% in May. Since then, the two largest economies are working on an agreement.

Besides escalating tariffs, structural shifts in sourcing strategies - including transshipment through Southeast Asia and Mexico - and reduced demand amid trade uncertainty have together driven this sharp drop in US imports from China.

Spotlight on China – Tech and machinery hit hardest

While China’s total export volumes are holding up, sector-specific pressure suggests that some Chinese firms are beginning to feel the pinch. The data reveals a marked decline in US imports of electronics and industrial machinery from China beginning in early 2025, coinciding with heightened trade frictions. Imports of electronics and industrial machinery fell by more than 60% in June compared to January 2025, reversing the late-2024 inventory build-up, which had been particularly strong in electronic equipment.

Notably, the decline in shipments began well before the reciprocal tariff regime came into effect in early April. Many US importers had already scaled back orders from China in February, when a 10% tariff was imposed. The prospect of additional increases - alongside uncertainty over the outcome of ongoing trade negotiations - prompted companies to act early, aiming to minimize supply chain exposure and shield themselves from unpredictable cost escalations.

Tariff uncertainty prompts preemptive rerouting of imports

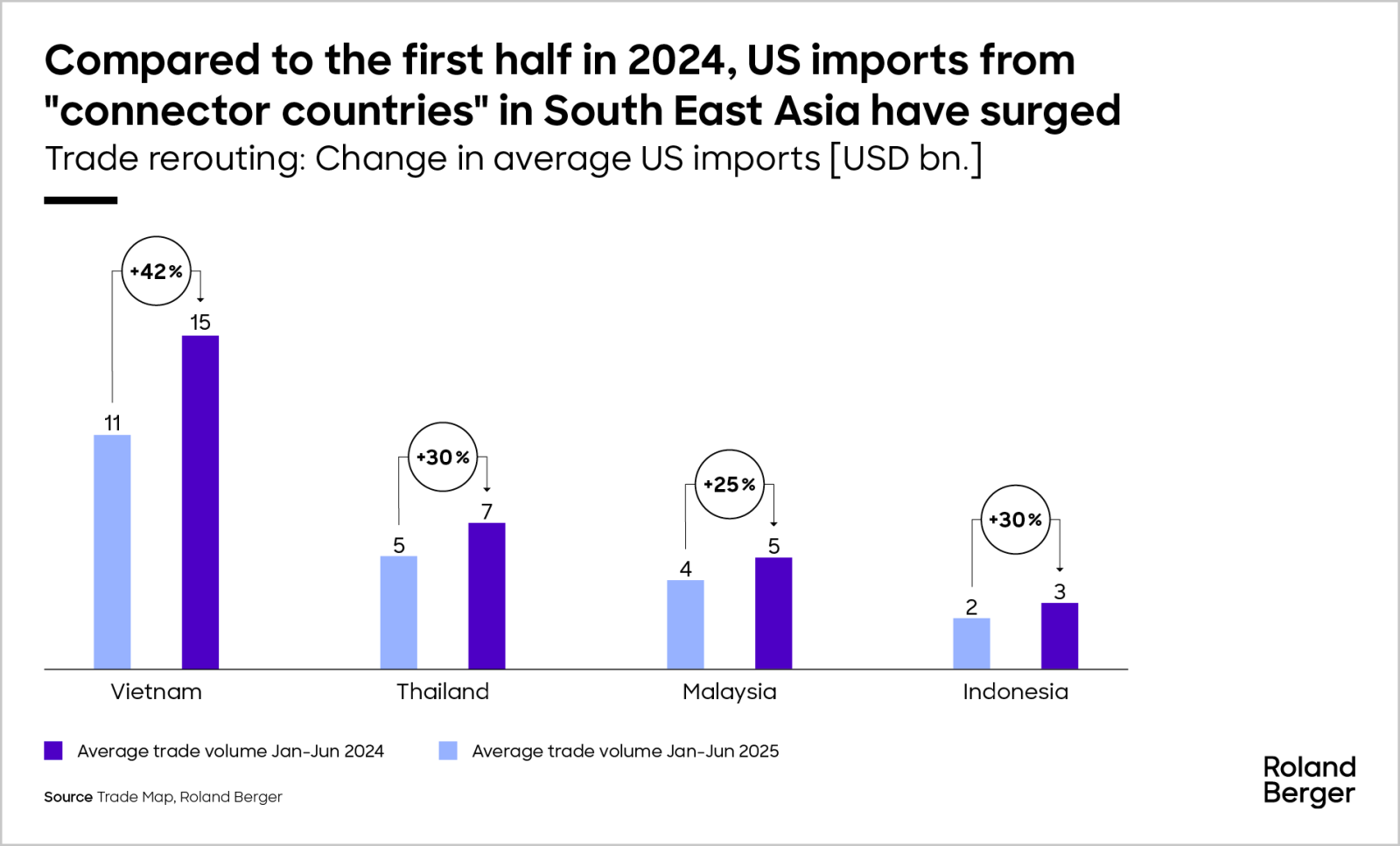

This anticipatory adjustment is part of a broader trajectory. Chinese exports to the US have already trended downwards since 2022, with a notable acceleration in the downturn starting in January 2025. The expansion of tariffs in April thus intensified an already ongoing decoupling trend. While imports from China dropped sharply, US importers have increasingly sourced products from Southeast Asian economies (and Mexico). Since Trump’s inauguration in January, shipments from countries such as Vietnam, Thailand, and Malaysia have spiked compared with the same period a year earlier.

The uncertainty around the final effective tariff rate to China, which was consistently higher than those applied to other Southeast Asian economies, appears to have prompted importers to diversify preemptively to countries that were perceived as less exposed to new duties. Thus, uncertainty and Trump’s focus on China have contributed to the rerouting of trade flows.

This mirrors the trade rerouting seen during Trump’s first term, when buyers pivoted toward alternative suppliers facing lower effective tariffs rates and fewer anticipated trade barriers than China. This time, however, the Trump administration has already signaled a tougher stance, announcing plans to impose additional tariffs on so called ‘transshipments’. Moreover, several Southeast Asian currencies have appreciated significantly against the US dollar following the introduction of tariffs, thereby further reducing the incentive for transshipment. However, the foreign exchange landscape remains mixed: while currencies such as the Thai Baht, Malaysian Ringgit, and the New Taiwan Dollar have strengthened considerably, others, including the Vietnamese Dong and the Indian Rupee, have depreciated.

Overall, the data signal a rapid reshaping of US trade flows. Tariffs have incentivized a shift away from China and Canada while boosting suppliers in Mexico and increasing shipping volume from Southeast Asia. Whether this reorientation endures will depend on the length and magnitude of tariffs and the resilience of new supply routes.

Sign up for our newsletter

Further readings