Roland Berger advises the aerospace, defense and security industries. We support OEMs, suppliers, agencies and investors.

Turbulent times in Aerospace MRO

How the aerospace aftermarket can recover from the corona crisis

The coronavirus crisis has left the aerospace MRO industry in turmoil, with a predicted market contraction in 2020 of up to 60%. In this article we revisit potential recovery scenarios in the industry and use our model to predict how different segments will fair in the future. We find that recession is now the most likely outcome – and consolidation the most likely solution.

The aerospace industry enjoyed strong growth between 2014 and 2019. But the coronavirus crisis has plunged it into turmoil and smashed further growth projections like a passing hurricane. Six months after the global industry all but shut down due to the pandemic, it is still in a perilous state. Although Europe and much of Asia have slowly begun ramping up economic activity, many big markets are still in thrall to the virus, including the USA, India and Brazil. The whole sector also remains at grave risk of a second wave of infections that will further prolong the downturn.

Despite this, airlines around the world are gradually resuming services. But in the absence of data to accurately predict demand, they are struggling with capacity planning. As a result, different carriers are employing different return-to-service strategies. Many have dropped flight change fees, and new business models are emerging, such as Emirates' COVID-19 insurance. Such moves and strategy variations reflect the ongoing uncertainty.

In this article, a follow up to a first article in April, we focus specifically on the effects of the coronavirus on the aerospace MRO industry. We forecast the potential financial impact over the coming years, and outline how we believe the industry will adjust to the ‘new normal’. We anticipate this will be a balance between recovered demand for air travel and new requirements around physical distancing, sustainability and de-globalization.

Recoveries revisited

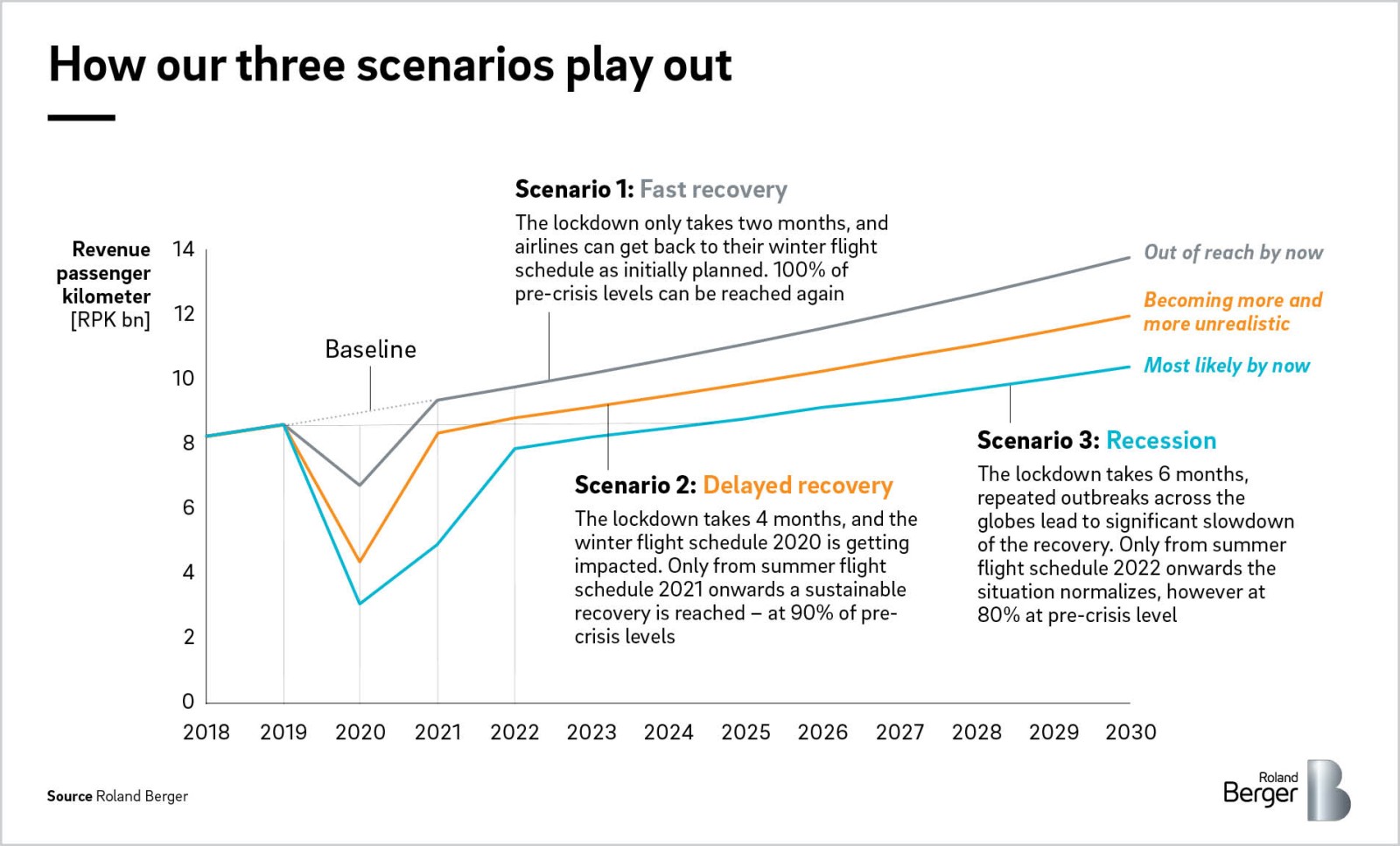

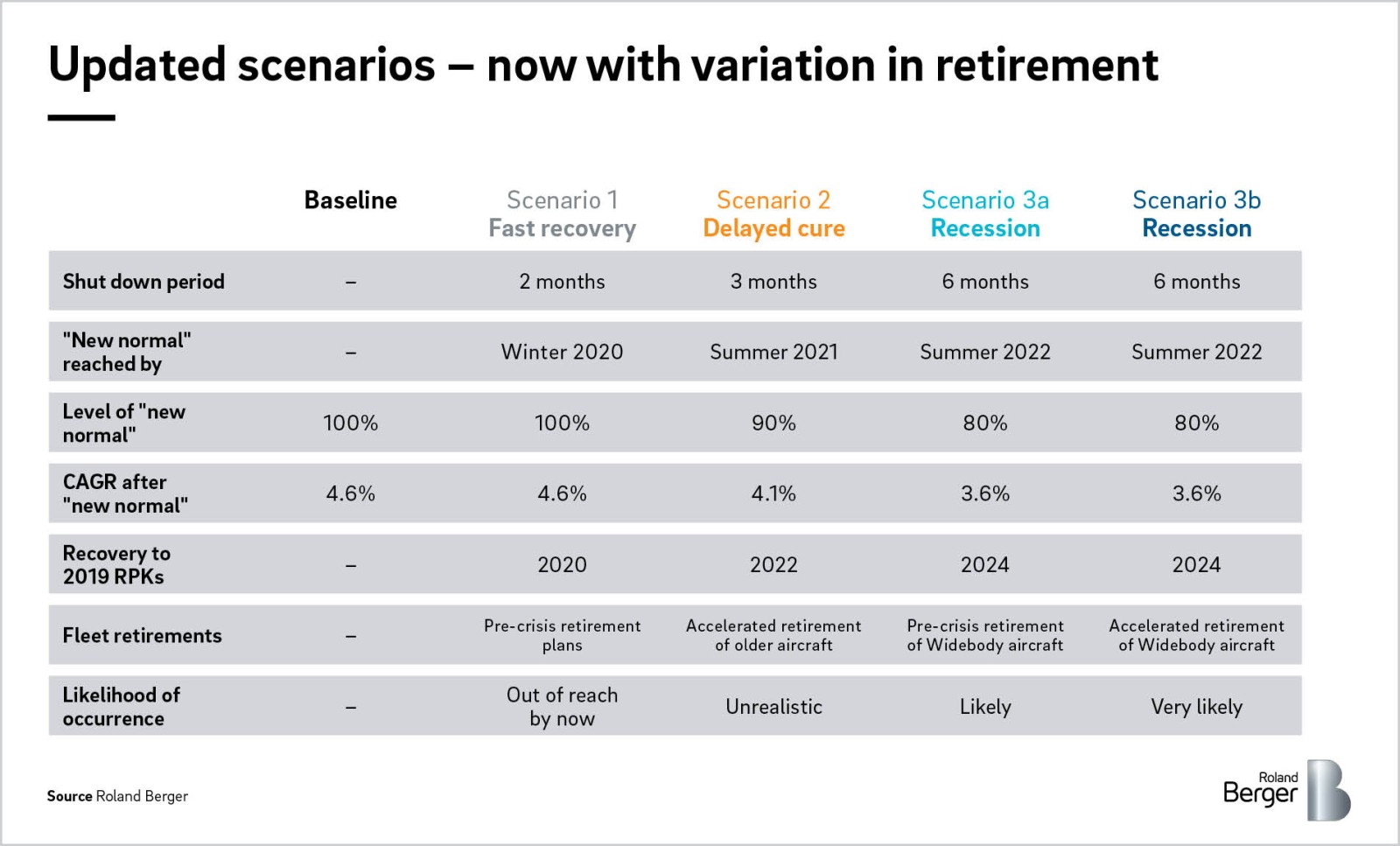

In April, as the pandemic became established worldwide, we set out three possible recovery scenarios: "Fast recovery", "Delayed cure" and "Recession". A "Fast recovery" was ruled out by June, and now we have to face the fact that a "Delayed cure" scenario is increasingly unlikely. Indeed, the "Recession" scenario is looking more and more likely, and it is the scenario we focus on in this article. To improve our analysis and factor in the growing rate at which airlines are now retiring aircraft, we split the scenario into two: "Recession" with retirements according to pre-crisis retirement plans (scenario 3a), and “Recession” with faster retirement of aircraft, specifically widebody aircraft (scenario 3b).

1. How COVID-19 will affect the MRO industry

A double hit for the market

Over the past weeks, more and more airlines have announced that currently grounded widebody aircraft, especially those of older generations such as Airbus A380s and Boeing 747s, will not return to service. This includes those that have not yet reached their regular end of life. We assume they will be replaced with new generation widebodies, such as Airbus A350s and Boeing 787s, or even long-range single aisle aircraft, such as the Airbus A321XLR, on specific routes.

This will come as a welcome boost for aircraft OEMS and their suppliers. But it represents a double hit for the MRO segment.

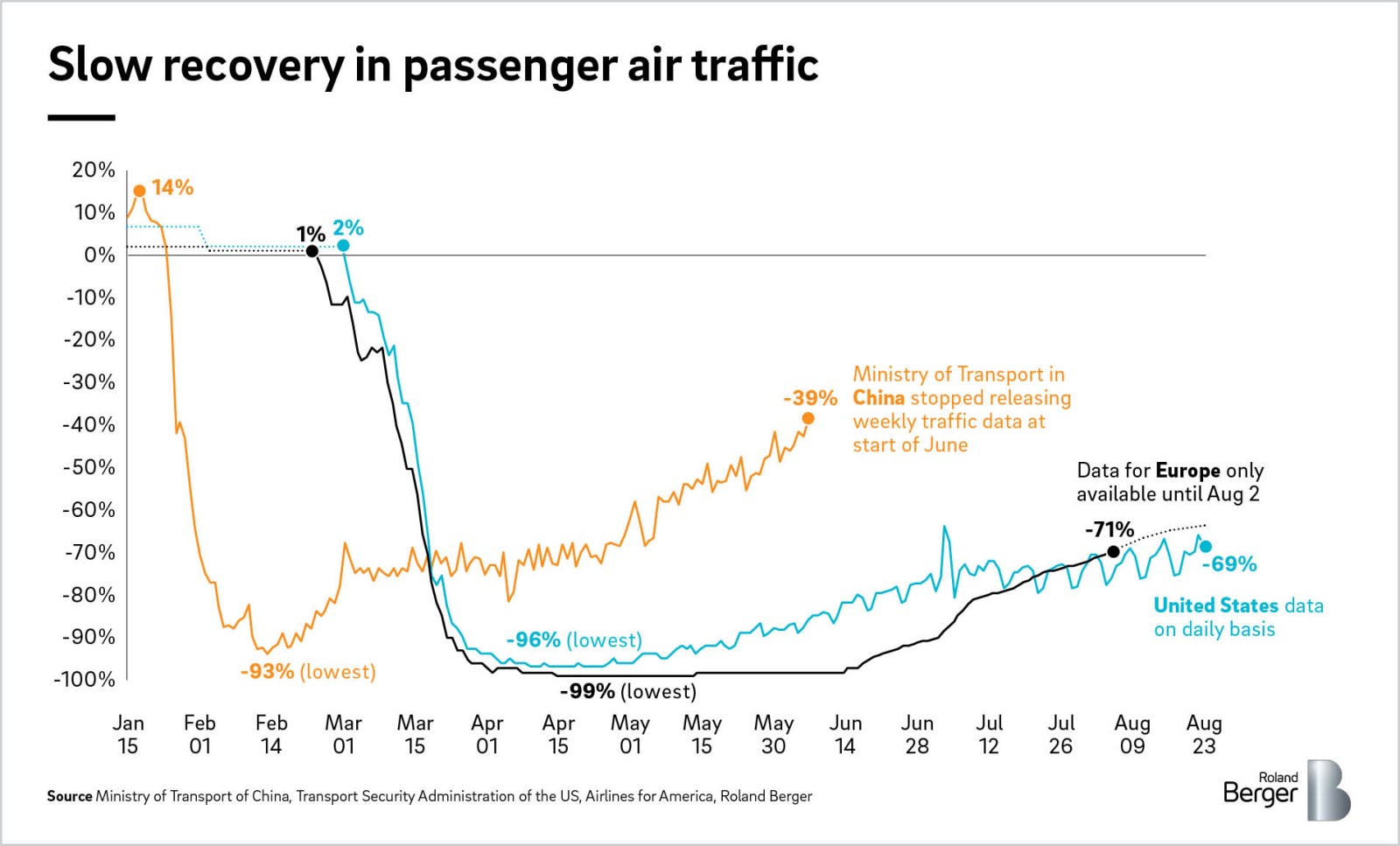

First, as the key driver for airline MRO spending is flown capacity (best measured in available seat kilometers, ASK, for passenger aircraft and available ton kilometers, ATK, for freighter aircraft), mass groundings have hit earnings hard. Up to 80% of regional fleets were taken out of service at the height of the outbreak between February and April, and although there has been some recovery since May, the return to normal remains slow. Past aviation crises, such as the global financial crisis in 2009, SARS in 2005 or 9/11 in 2001, showed that MRO spending is highly sensitive to changes in ASKs – for every 10% change in ASKs, MRO spending varied by 12-18%. With the severe reduction in ASKs due to the COVID crisis, we anticipate a dramatic short-term drop in the aftermarket in 2020. Key players in the segment reported a downturn in revenues of 50-70% in Q2 2020, for example.

Second, aircraft in the second half of their life (10 years plus) account for an above average share of MRO spending as they start requiring heavy maintenance checks. If these older planes are retired and replaced with new aircraft, this MRO work is gone and will only come back once the new aircraft reach their first heavy maintenance cycles.

Another factor is also at work. In order to keep some routes operational and to manage flights in accordance with physical distancing requirements, airlines face significant drops in load factors. This will mean a fall in revenue passenger kilometers (RPK) that is even more dramatic than that in ASK. Airlines will try to minimize maintenance costs as a result, meaning MRO revenues will come under enormous pressure. MRO players are expected to react by adopting massive cost cutting measures, including reducing temp labor, layoffs of permanent employees in operational and administrational functions, and scaling down of operations.

Impact model and results

To predict the impact on the aerospace aftermarket in detail, we used our fleet-based MRO spending forecast model to generate scenarios of how MRO spending – and thus revenues for aftermarket players – will be affected in the short and longer term. It considers individual aircraft types at platform level, broken down regionally and by age, thereby differentiating between geographic and age-related aftermarket spending. This allowed us to tailor-make strategies for our clients.

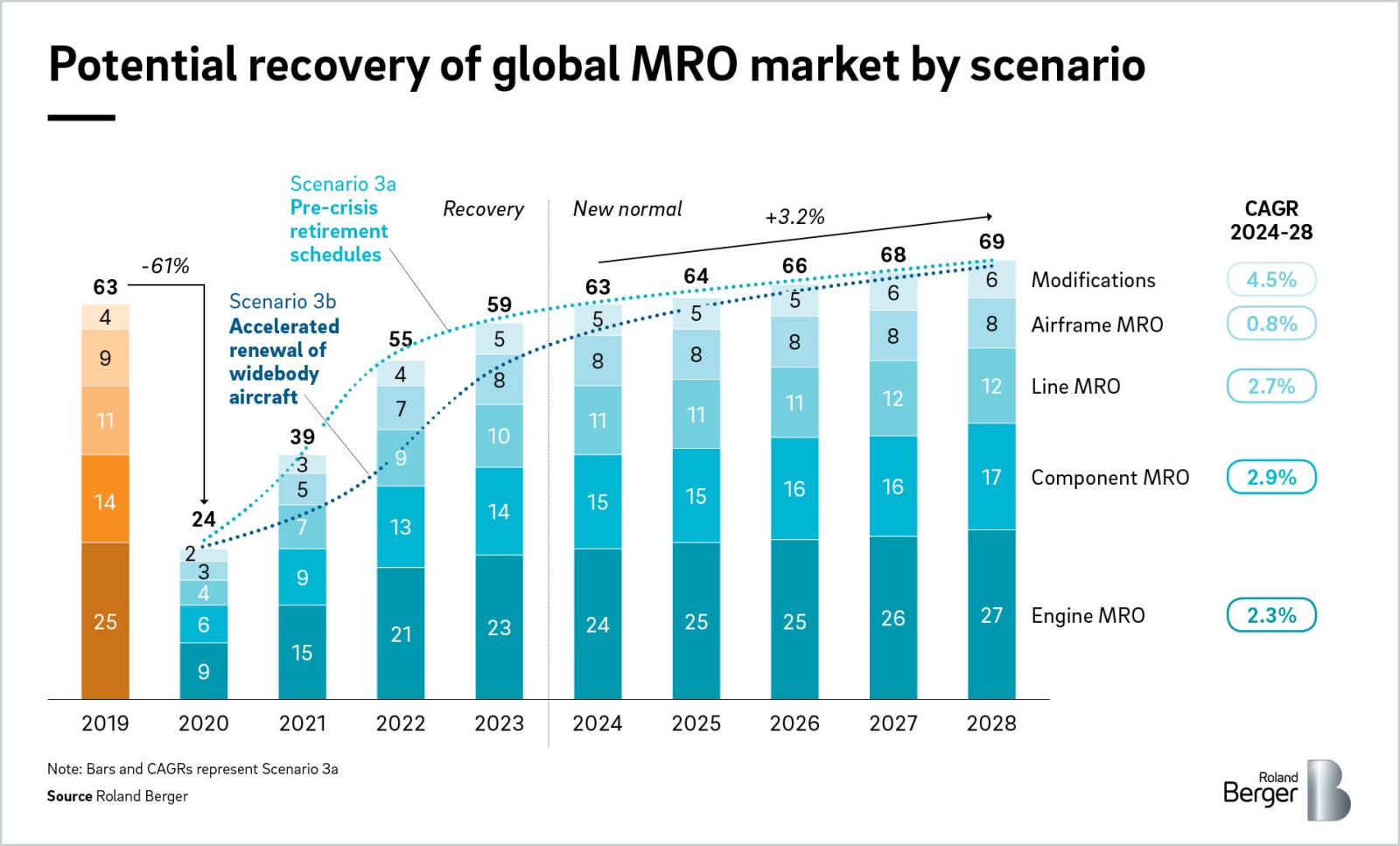

We modelled “Delayed cure” and both “Recession” scenarios. The results showed a contraction of the global MRO market of between 60% and 75% in the first half of 2020, depending on the scenario. Over the whole of 2020, the drop was greatest for the “Recession” scenarios, with little difference between scenario 3a and 3b – 3a forecasts a fall of 61% from the 2019 base level of EUR 63 billion to EUR 24 billion, and 3b a fall of 63% to EUR 23 billion. The “Delayed cure” scenario fell 46% to EUR 34 billion. However, the different retirement/ fleet renewal strategies do impact recovery in the years beyond 2020. Accelerated renewal of older aircraft by new generation aircraft leads to delayed recovery in the MRO sector as the new aircraft require less MRO spending.

Effects on individual sub-segments

The impact of COVID-19 on each sub-segment of the MRO industry varies according to the nature of their business:

- Line maintenance: Line maintenance is directly linked to the number of flight cycles, which in turn correlates to ASK if average leg distance remains unchanged. As such, the demand for line maintenance dropped by the same magnitude as ASKs, and is also expected to ramp-up at nearly the same pace. There may be a slight lag as airlines are expected to opt out of optional elements of line maintenance wherever possible.

- Airframe maintenance: This segment is expected to be hit exceptionally hard by the downturn. Aircraft that were close to a heavy check have been prioritized for grounding and those in the second half of their life may not return to the fleet or may be replaced by new aircraft. On top of this, airlines will try to postpone heavy checks by optimizing useful life across the fleet. Recently, it has become common to split heavy checks (C/D checks) into smaller chunks to better manage fleet capacity, and this may help to counter the expected downturn in airframe maintenance. However, we believe that overall, this segment will be hit above the ASK average downturn.

- Component maintenance: This segment is expected to show hybrid behavior. The MRO of life limited components is linked to flight cycles, hours or other mandatory replacement limits, while other components can be maintained based on their actual condition. Another factor here is the availability of useful components from grounded aircraft that won't go back to service. As some of those aircraft will be retired earlier than planned, the value of their components will be higher than expected and they will be made available on the spares market. We therefore expect this segment to recover slightly more slowly than ASK, but it is not expected to suffer as much as airframe maintenance.

- Engine maintenance: This segment is expected to be hit hard in the short term as airlines will maximize the useful flight cycles/ hours of their engines. They will also have a higher number of green time engines available from grounded aircraft, which they can use to further exploit their engine pool. In addition, airlines can start parting out engines of aircraft that won't return to the fleet for Used Serviceable Material (USM), reducing demand for spares and putting pressure on engine OEMs. This practice will be limited, however, by flexibility constraints across different aircraft types and routes. In the long term, this segment will suffer strongly from accelerated fleet replacement. Last generation engines powering aircraft, such as the Airbus A340 and A380, and Boeing 747 and 777, contributed significantly to MRO spending prior to the crisis, and their earlier-than-planned replacement with new generation engines will hit this hard.

- Modifications: This segment is expected to gain importance through the crisis. Cabin modifications to install new health and disinfection measures, such as HVAC upgrades, antibacterial surfaces or touchless cabin elements, are expected to create additional demand. However, the realization of these new features will take some time as they are still in development, and airlines will lack cash to pay for them, at least for the next 1-2 years.

Effects on individual regions

We expect some notable regional differences in market recovery. Spending by airlines in Asia Pacific is forecasted to bounce back most rapidly, returning to 2019 levels by late 2022. The prognosis for Latin America and Africa remains very unclear, with a greater risk that the coronavirus crisis will last longer in these regions. Current projections suggest a recovery to 2019 levels by 2023, but with high uncertainty. The recovery in Europe and North America is expected to be much slower, the result of weaker general demand growth, such as the increased ability for potential business travelers to switch to remote working. Spending by European airlines is expected to return to 2019 levels only by 2024, while North American spending may recover as late as 2025. Overall, domestic and regional flights are likely to ramp up faster than intercontinental traffic, which will remain constrained until international travel restrictions are lifted.

2. Predicting the future of the MRO industry

Consolidation looms

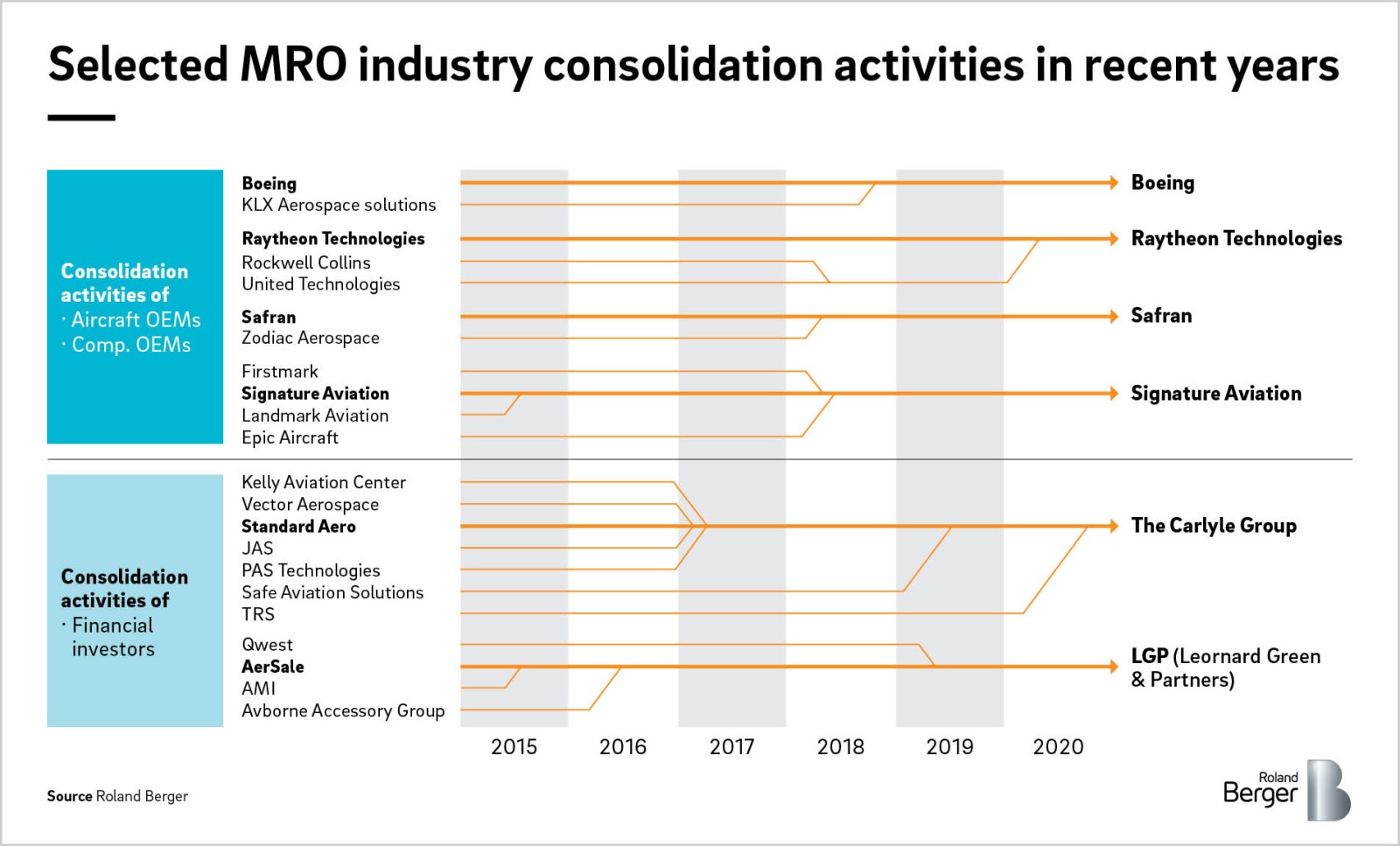

With difficult years ahead, the industry needs to act. In the short term, traditional cost-cutting measures, such as workforce flexibilization, spend compression and postponement of investments, have been applied by nearly all players, and governments have stepped in with financial support. However, as the downturn is expected to last for at least 2-3 years, mid- to long-term effects such as market dropouts, takeovers and industry consolidation seem inevitable. Considering that the aerospace supplier industry has seen significant consolidation moves in the past, consolidation in the MRO segment is likely in the coming months and years.

Cases like the two-step consolidation of supplier giants United Technologies, Rockwell Collins and Raytheon into Raytheon Technologies clearly show how the combining of forces can lead to a very strong position in the aftermarket. Equally, the integration of Zodiac Aerospace into Safran shows how leading players can gain strength by acquiring other companies to expand their value-chain coverage. Financial investors have also been active in the MRO segment, most prominently The Carlyle Group with its "buy and build" strategy, clustering companies around their leading asset StandardAero. Aircraft OEMs have been rather selective so far, focusing on specific areas like parts sale. Both Airbus and Boeing have strengthened their spare parts distribution segments, Boeing with Aviall in 2006 and KLX in 2018, and Airbus with Satair in 2013. In addition, both companies are considering insourcing of selected systems activities to get better access to the aftermarket.

Consolidation motivations of different industry groups

To anticipate future structural changes in the MRO industry, we analyzed the motivation and general direction of business focus and consolidation of six different company groups.

- Aircraft OEMs are looking at alternative sources of revenue as new aircraft sales have fallen significantly. Stronger control over the aftermarket combined with digital services could help to build resilient revenue streams.

- Engine OEMs typically work with a broad network of smaller suppliers to serve the aftermarket. But in the current crisis, we expect them to do more work inhouse to keep their own shops utilized, thus putting significant pressure on independents.

- Component OEMs typically leverage the aftermarket for their components quite well. However, they could seize the opportunity to acquire small/ medium sized players to increase their product and service portfolio.

- Airline inhouse MRO business is expected to come under additional pressure, driven by crisis-triggered consolidation in the airlines' market. Airlines may be forced to divest their captive MRO activities to free up cash and manage their survival. Some strong inhouse MRO shops could benefit by gaining higher shares of third-party business.

- Independent MRO providers are expected to be hit hardest by the crisis. As outlined above, component OEMs are expected to take work back inhouse which will put tremendous pressure on independent MROs. On the other hand, surviving independents will have the opportunity to acquire distressed competitors and expand their service portfolio and/ or their regional footprint.

- Financial investors are likely to seize the opportunity to acquire distressed assets, either as pure financial investment or to consolidate key players into new, market leading independent providers. One critical issue for financial investors will be to manage license issues due to change of ownership clauses. In contrast to strategic investors, which may be able to transfer MRO licenses to their own MRO organization, financial investors will need to find ways to manage this issue, for example by first acquiring one leading asset which can then be used to take over licenses from subsequent assets.

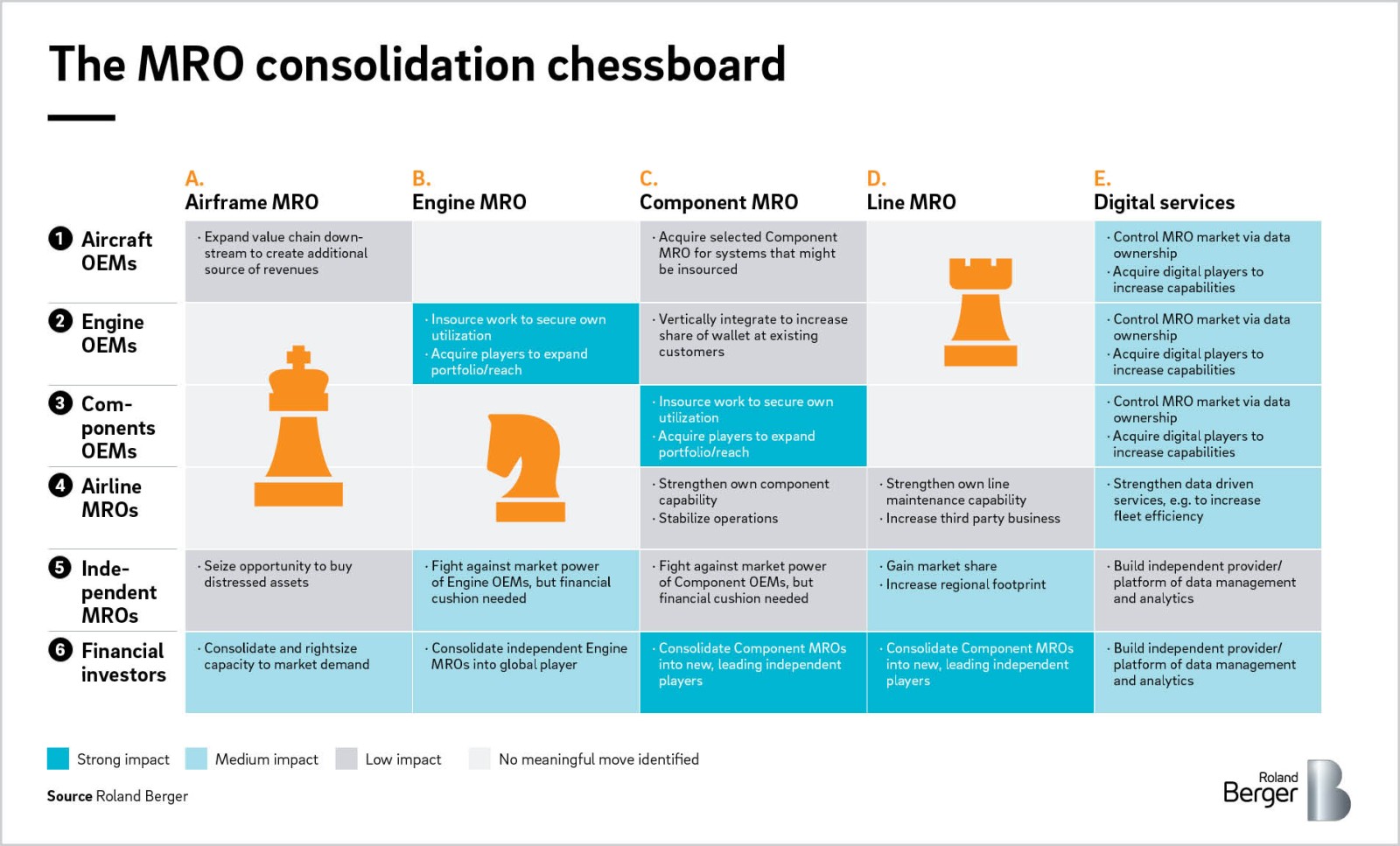

Potential consolidation outcomes for industry groups

In addition to this high-level assessment, we created the MRO consolidation chessboard. It maps the six previously defined group of actors with the potential segments of consolidation, and outlines the rationales per actor group to strengthen the business in specific segments, or even enter new segments. Although the rationale for each individual case of an acquisition or any other form of consolidation will strongly depend on the involved players and their specific situation, there are some common schemes implying scripted moves on the chessboard. Areas with an expected strong impact and high probability of action have been highlighted in dark blue, areas of medium impact and probability in light blue and areas in which we expect to see only selected moves in light grey.

Based on this structured analysis, we believe that:

Aircraft OEMs will play only a minor role in the MRO consolidation game. Their key move may be to strengthen their power position by stronger control of the aftermarket via digital services and related data ownerships. This will ensure that new MRO services are in line with their development vision and are being executed in a controlled environment. In terms of M&A activity, we expect them to remain focused on specific segments, such as parts or specific systems, which they intend to add to their capabilities

Engine and Component OEMs are expected to play a key role within their current business perimeter. On top of insourcing work to keep their own MRO shops utilized, they can play the traditional consolidation game of acquiring MRO players for pure market share or technology expansion reasons, and can increase their control via IP or data ownership means.

Airline MROs will have a hard time playing an active role in the game. They will be hit by airline consolidation and surviving airlines will try to optimize their MRO cost at the ‘new normal’. Divestment of inhouse MRO services may be a potential means to realize those cost savings. Only the survivors of that game will get the chance to take over third-party work from other airlines.

Independent MROs could benefit from the above-mentioned cost reduction pressure if they have the financial means to expand and take over third-party work for airlines that outsourced their MRO services. On the other hand, competitive pressure will hit them as well, so they need to carefully plan those moves

Financial investors seem to be the most versatile player in the game. Having financial means helps, of course, to play the game the right way and opportunities will arise, for example to consolidate in the engine, component or line maintenance segment. Entering the digital side of the business playing the "neutral owner of data" card could be a powerful move and a gamechanger in this segment.

Conclusion – From COVID to consolidation

The coronavirus crisis has plunged the aerospace industry into the biggest downturn in its history, and MRO is expected to be among the most hit segments. There are clear indications that the industry will stabilize on a lower level and with a reduced number of players compared to pre-crisis projections. Yet a positive momentum can be gained from the crisis, a momentum towards a more sustainable, more innovative and more ecologically oriented development. The consolidation moves and structural changes outlined in this paper will contribute to the renewed innovation power of the industry. The coming years will not be easy and there will be losers in this transformation. But companies that take action by becoming a driver of the "MRO consolidation game" will find ways to manage the challenges ahead and enter the era of the 'new normal' as winners.

Our Global Network

Germany

Further readings

All publications from this series