Internationally operating auto parts distributors are already leading the pack and shaping the European market. Boasting annual revenues of over a billion euros coupled with stable growth, they have the necessary scale, purchasing power and distribution strength. Unsurprisingly, their EBITDA margins of four to five percent position them at the top end of their industry peers. Smaller companies with up to 100 million euros in revenues manage just two to three percent margin, by contrast. This puts them under particular pressure in the market and more of them go bust as a result: the number of insolvencies rose nine percent between 2016 and 2017 alone.

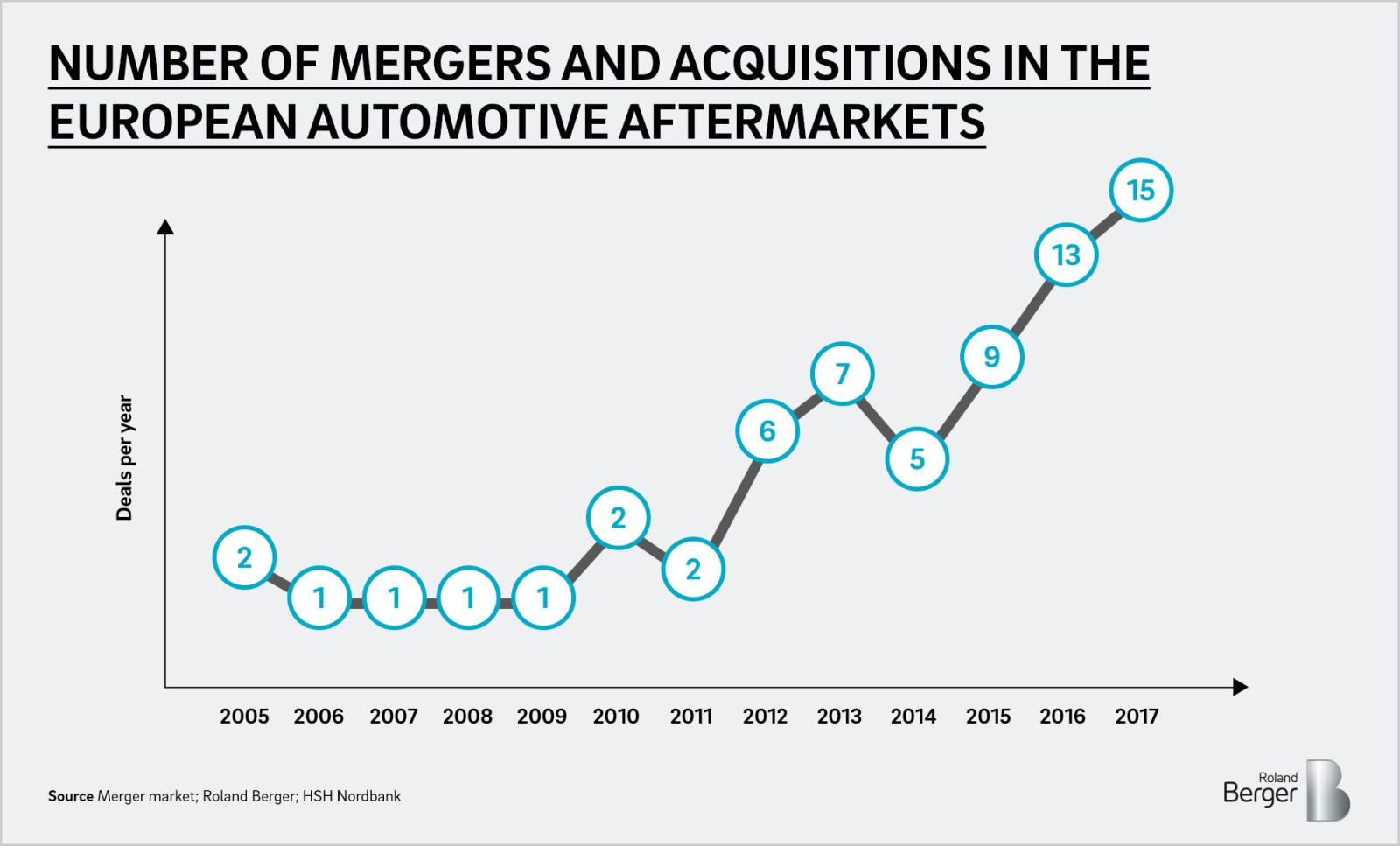

Most of the mergers and acquisitions are undertaken by strategic investors keen to improve their own position on the market, develop new markets or realize economies of scale. Another reason for the increase in M&A deals in the sector is the presence of financial investors: there has been increasing involvement of private equity firms in the market since 2012 because of the good-value investment opportunities to be found in the industry.

Active players profit

The consolidation phase is not expected to end any time soon – quite the reverse, in fact. Market players must therefore ask themselves how they can use the disruption within their industry to evolve their own businesses. Opportunities abound, not only for the big players doing the acquiring, but also for the targets, for reasons including the fact that they will emerge from a merger stronger than before as a result of economies of scale.

The first thing companies should do is keep a close eye on what's going on in the market and analyze the options open to them. Questions they need to ask themselves include: How big is my business and where do I fit in to the market? Can I acquire a rival firm myself? What is my value chain like – do I need to add or get rid of certain links? What strategy promises success in dealing with new players such as online platforms and in the face of digitalization? Are there potential partnerships or investments to be entered into? Based on the answers to these questions, companies can develop and implement measures such as changes to the product and service portfolio, establishment of the online business, joint ventures or a strategy of expansion.

The key is to develop an awareness of the best course to chart to successfully ride the consolidation wave. Companies need to be agile and open to changes because they must not allow themselves to freeze like rabbits in the headlights. They need to take the future of their business in their own hands. Then they will emerge the stronger for all the disruption in the automotive aftermarket today.

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/Roland_Berger_Aftermarket_Studie_Cover_EN_download_preview.jpg)