Study

PSD2: Bumpy Start for Open Banking

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/Roland_Berge_STU_553_PSD2_cover_download_preview.png)

PSD2: The vast majority of European banks see the Payment Services Directive as an opportunity - but there is still a wide gap between ambition and reality.

Published December 2019. Available in

The vast majority of European financial institutions (81 percent) see the second Payment Services Directive (PSD2), which came into force in the EU on September 14, as an opportunity. However, most banks are still reluctant to take advantage of the new opportunities: only around one third (35 percent) of banks have so far positioned themselves to take on the role of a third-party provider. These are the key findings of Roland Berger's study "Adapt or die? Why PSD2 has so far failed to unlock the potential of Open Banking". The publication included interviews with over 40 leading banks, third-party providers and large technology companies in twelve European markets.

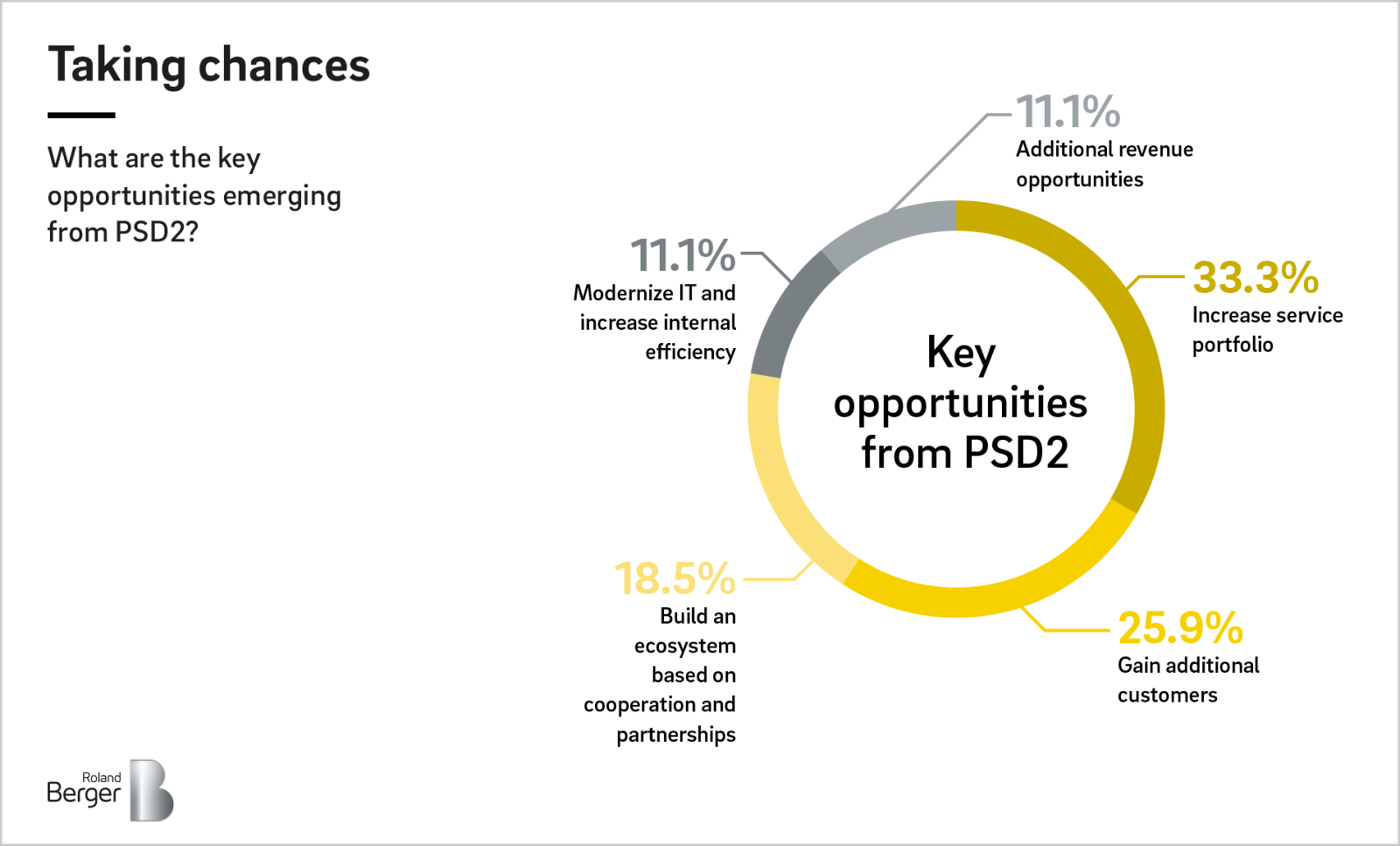

In addition to greater consumer protection and payment security for customers, the PSD2 means heightened competition for banks – they are now obliged to provide third-party providers access to customer data. On the other hand, the PSD2 also opens up new strategic opportunities on the way to an EU-wide open banking scenario. Finally, PSD2 allows banks to enrich their already plentiful customer information with even more external data. As such, almost three-quarters of banks (72 percent) plan to improve their service portfolio with PSD2 and, in doing so, attract new customers. However, most of the banks have not yet reached that stage and are initially focusing on meeting the minimum statutory requirements.

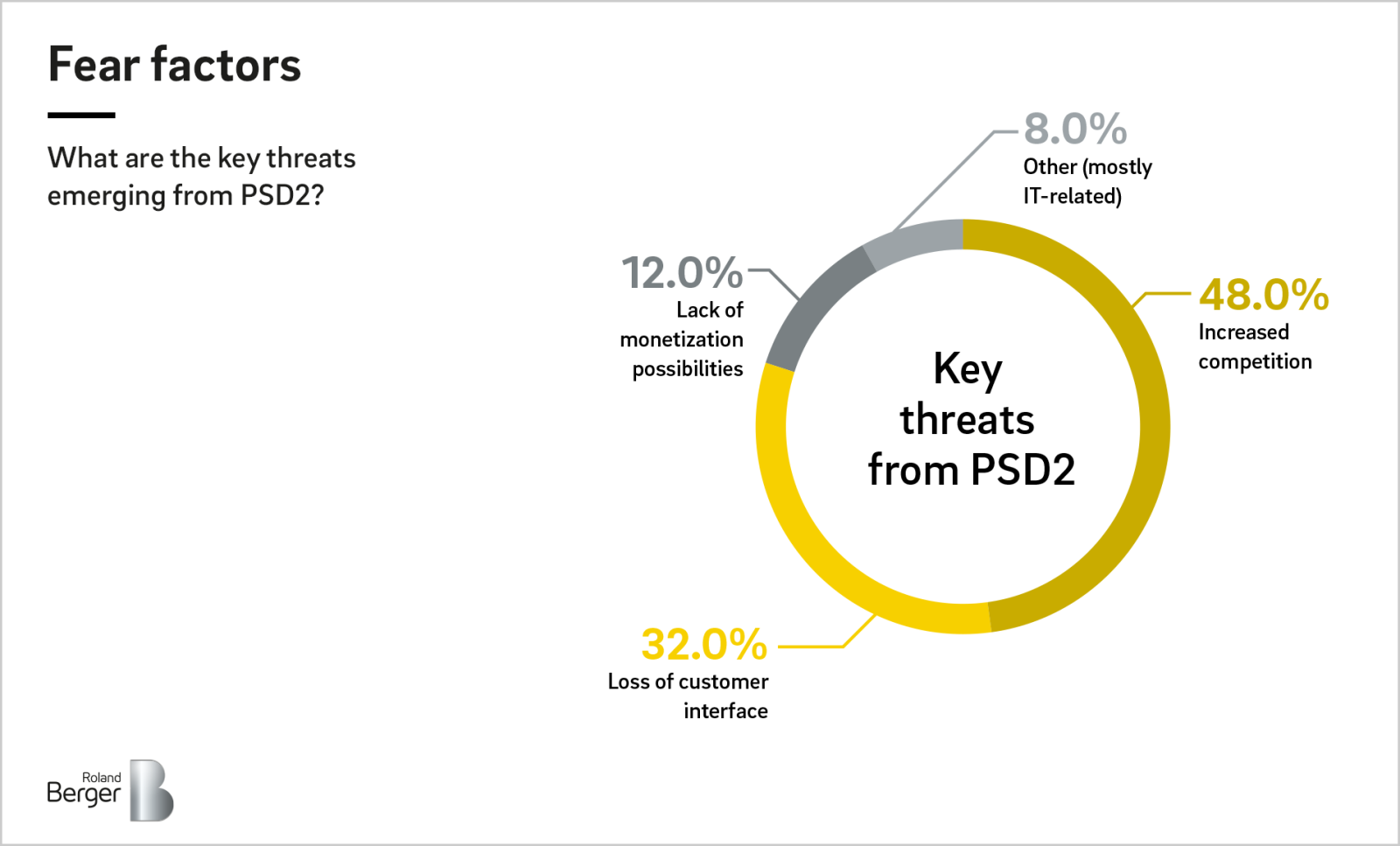

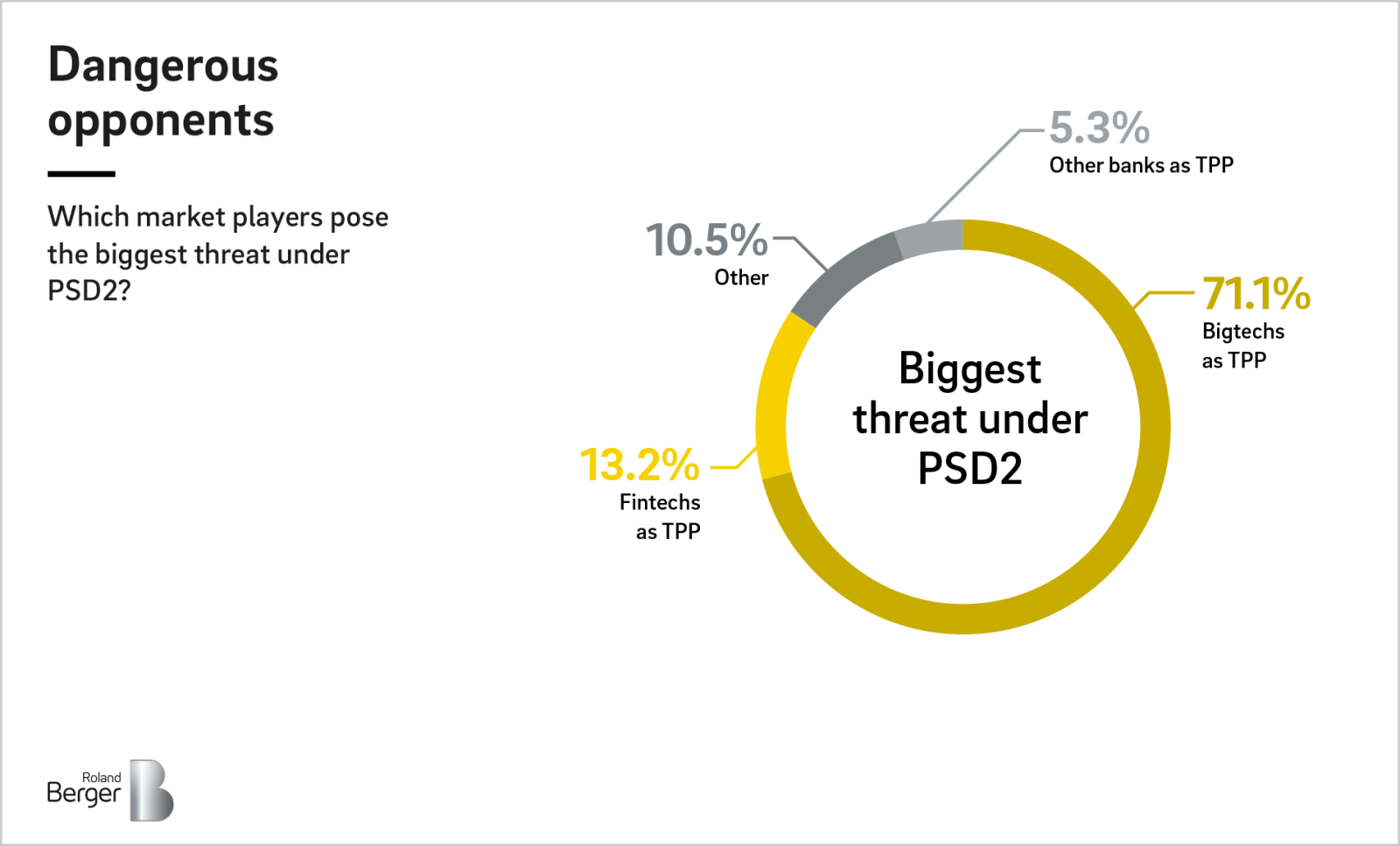

One thing is clear - the banks' hesitation in implementing PSD2 is largely due to the extremely difficult market environment: low interest rates, stricter regulation and outdated IT infrastructure are just some of the challenges. However, financial institutions cannot afford to ignore the opportunities offered by PSD2 as there is a danger that this gap will be filled by new financially strong competition. The banks understand this: 54 percent of interviewees believe that their high level of customer trust offers strong protection against other players and see this solid basis as an advantage against the competition. Nevertheless, they are aware of new competitors entering the market and threatening their business models: first and foremost, large technology groups (71 percent) such as Google, Amazon, Facebook and Apple. FinTechs, on the other hand, are seen by established service providers as partners rather than competitors.

PSD2 marks the entry into an open banking scenario in which established financial service providers grant other companies access to data and cooperate together - always with the aim of offering customers better products and services. After all, 80 percent of study participants regard open banking as a top management priority in their companies. Depending on the bank's business model, this scenario can have very different effects. New opportunities are opening up, especially for smaller institutions that specialize in specific areas. In the world of open banking, they are in a position to make their products available to a much wider clientele and subsequently achieve higher revenues.

Open banking will change the value chains in the financial industry dramatically and all players will have to adapt quickly. First of all, this involves working out a clear strategic positioning. In the future, no institution will be in a position to alone offer all services. European banks still have the opportunity to proactively seize these opportunities. PSD2 has created the framework, now it is up to the banks to fill it.

The Payment Services Directive 2, PSD2 for short, is an EU-wide directive regulating payment services and payment service providers. The PSD2 is characterized by three essential components: increased consumer protection, which has been in effect since January 2018; greater payment security, which is to be achieved through the introduction of the so-called "Strong Customer Authentication"; and competition and innovation in the market. A crucial element of PSD2 is the opening of account interfaces to third party providers in order to promote competition and innovation in the banking sector.

PSD2: The vast majority of European banks see the Payment Services Directive as an opportunity - but there is still a wide gap between ambition and reality.