AI is reshaping global data center infrastructure. Roland Berger experts examine the data center boom, its correction risks, and what Europe must do to compete.

Water demands of the data economy

By Geoff Gage and Bill Malarkey

Four strategic shifts to secure water access in an era of digital growth

As enterprises accelerate their digital transformation - scaling AI workloads, expanding cloud infrastructure, and processing exponential data volumes - they're driving unprecedented demand for data center capacity. But this growth comes with a resource constraint that few boardrooms are discussing: water scarcity. For business leaders managing large-scale digital operations, understanding the water-energy nexus isn't just an ESG concern, it's becoming a material business risk that could impact operational continuity, regulatory compliance, and stakeholder relations.

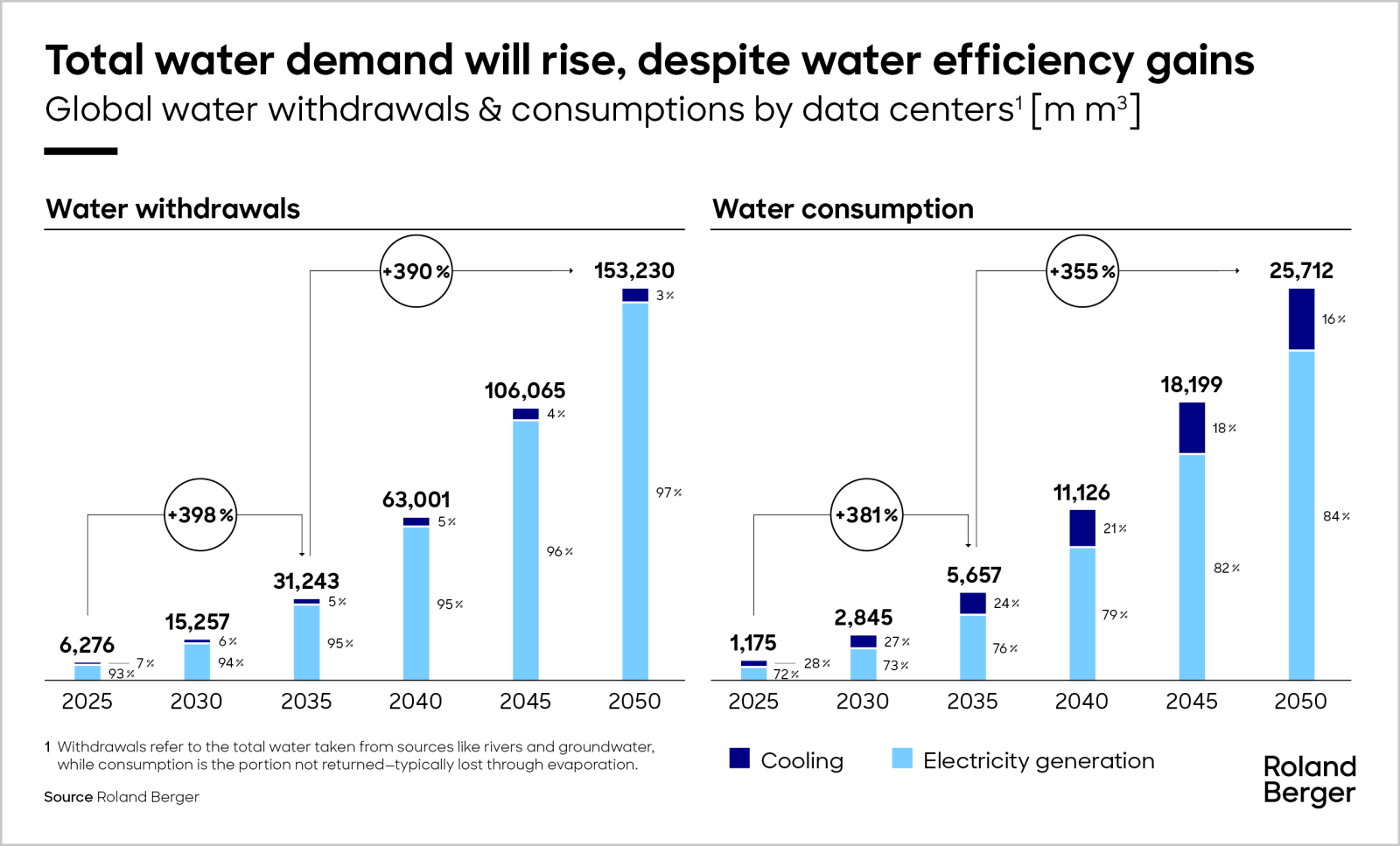

Data’s dual water impact

"Next-generation cooling technologies can reduce water consumption, but absolute water demand will continue rising; efficiency gains won't offset exponential growth."

Most enterprise technology leaders focus on driving data center energy efficiency and reducing their carbon footprint. However, water consumption represents a less visible, but equally critical, operational dependency. The water footprint of data center operations breaks down into two categories:

Direct water use (15-30% of total): Conventional liquid cooling infrastructure relies on water-based systems, with cooling towers and evaporative processes consuming water to maintain optimal operating temperatures for compute infrastructure.

Indirect water use (70-85% of total): The larger, often invisible impact comes from electricity generation. Power plants supplying the grid require substantial water for cooling and steam generation - meaning your data center's energy demand translates directly into upstream water withdrawal.

For enterprises evaluating colocation providers or planning private data center buildouts, this 70 to 85% indirect consumption represents a blind spot in most sustainability assessments. Your Scope 2 emissions reporting likely captures energy, but are you tracking the embedded water cost of that energy?

Site selection: The water-energy trade-off

The data center industry faces a strategic dilemma. More than two-thirds of new facilities constructed since 2022 are located in water-stressed regions such as the Southwest US, Saudi Arabia, and India. This isn't accidental - it reflects a deliberate strategy that prioritizes land availability and energy economics over water availability.

For hyperscalers and colocation providers, these locations offer compelling advantages:

- Renewable energy abundance: Arid regions deliver superior solar irradiance and consistent wind resources, supporting corporate renewable energy commitments

- Land availability and cost efficiency: Expansive, low-cost real estate enables large-scale campus development

- Climate resilience: Stable weather patterns reduce operational risks from flooding, hurricanes, or extreme weather events

- Regulatory incentives: State and national governments often designate data centers as critical infrastructure, offering tax incentives and expedited permitting despite local water constraints

This creates a complex risk matrix for enterprise decision-makers. The immediate operational benefits, including lower energy costs, renewable energy access, favorable business climate, must be weighed against longer-term water availability risks, potential community opposition, and evolving regulatory frameworks around water use in stressed basins.

Efficiency gains won't offset growth

Enterprise digital transformation is driving unprecedented growth of the data center industry. While the specific degree of growth is uncertain due to technological shifts, cost elasticity and supply chain constraints, among other factors, absolute energy and water demands will continue to increase, particularly as the number of data centers dedicated to AI solutions rises. Currently, AI queries require ~9x more energy than traditional Google searches.

For enterprises with significant data center footprints or those planning major capacity expansions, this creates several strategic implications:

- Operational risk: Water constraints could limit capacity expansion in preferred geographies

- Cost volatility: Water scarcity drives up utility costs and may trigger usage-based pricing models

- Stakeholder pressure: Investors, customers, and communities are increasingly scrutinizing water stewardship

- Regulatory exposure: Water-stressed regions may implement restrictions that impact operational flexibility

Four levers for water stewardship

Leading organizations are moving beyond aspirational sustainability statements to implement concrete strategies that reduce water dependency while maintaining operational performance.

Here are five potential interventions to consider:

1. Accelerate advanced cooling technology adoption

"More than two-thirds of new data centers constructed since 2022 are located in water-stressed regions - not by accident, but because land availability and energy economics are prioritized over water availability."

Next-generation cooling architectures, including direct-to-chip liquid cooling and immersion cooling, can reduce water consumption by 90% or more compared to traditional computer room air conditioning (CRAC) systems. While requiring higher capital investment, these technologies deliver lower total cost of ownership (TCO) through reduced utility costs and higher rack densities. For enterprises planning new facilities or refreshing existing infrastructure, evaluating water-efficient cooling should be a key selection criterion.

2. Implement closed-loop water treatment systems

On-site water treatment and recycling infrastructure creates closed-loop systems that can reduce freshwater withdrawal by 60 to 80%. Advanced filtration and treatment technologies enable multiple cycles of reuse, converting water from an ongoing operational expense to a managed, recyclable resource. This is particularly critical for facilities in water-stressed regions where withdrawal limits may constrain future growth.

3. Evaluate water-as-a-service provider models

Emerging service models allow enterprises to transfer water management accountability to specialized providers through performance-based contracts. These arrangements can include guaranteed water efficiency metrics, regulatory compliance management, and risk transfer mechanisms. For organizations where water management isn't a core competency, this approach allows focus on strategic technology priorities while ensuring professional stewardship of water resources.

4. Accelerate adoption of more holistic tracking metrics

The industry's focus on Power Usage Effectiveness (PUE) has driven meaningful efficiency gains but creates an incomplete picture. Forward-thinking data centers are also reporting on Water Usage Effectiveness (WUE), which typically tracks energy efficiency, water consumption on site and for energy generation, and carbon intensity - recognizing that these variables must be optimized as a system rather than in isolation.

From risk to competitive advantage

Enterprise digital demand will continue accelerating. AI workloads, real-time analytics, and expanding cloud adoption are non-negotiable requirements for competitive performance. However, this growth trajectory cannot ignore fundamental resource constraints.

Organizations that proactively address water stewardship aren't simply managing ESG reporting requirements — they're building operational resilience against regulatory restrictions, community opposition, and resource availability constraints that could limit future capacity.

Ankita Soni contributed to this article.

Sign up for our newsletter

Stay current with our latest insights on water, sustainability and climate action topics. We will email you when new articles and studies are published.

Further readings