A look at the market, use cases, risks and opportunities for players in the maritime ecosystem.

Autonomous shipping industry survey 2025

By Kiyoung Song and Christian Vinck

More remote control than full automation

The global autonomous shipping market is evolving slower than initially projected, with maritime industry professionals prioritizing remote controlled vessel operations over fully automated ships. This is one of the key findings of a comprehensive analysis of maritime automation trends based on a survey of more than 20 experts attending Amsterdam Marine Equipment Fair. The extensive survey of shipbuilding stakeholders reveals critical insights into the current state of maritime automation technology and its future trajectory.

Current state of autonomous shipping

For the maritime industry, the concept of autonomous shipping differs significantly from the idea of autonomous ground transportation. The survey revealed that 41% of industry professionals – including shipbuilders, suppliers, operators, consultants, and infrastructure providers – consider autonomous shipping to be "remote controlled" operations, while 29% define it as "partially remote controlled" systems and another 29% envision fully autonomous vessel operations.

With a clear preference for maintaining human oversight, reflecting legitimate concerns about the safety, regulatory compliance, and technological readiness of autonomous shipping, the shipping industry is evidently taking a more measured approach to autonomous operations than, say, the automotive industry.

The emphasis on remote control systems rather than full autonomy aligns with practical maritime realities, including the complexity of navigating through international waters, variable weather conditions, and the high-stakes nature of cargo transportation.

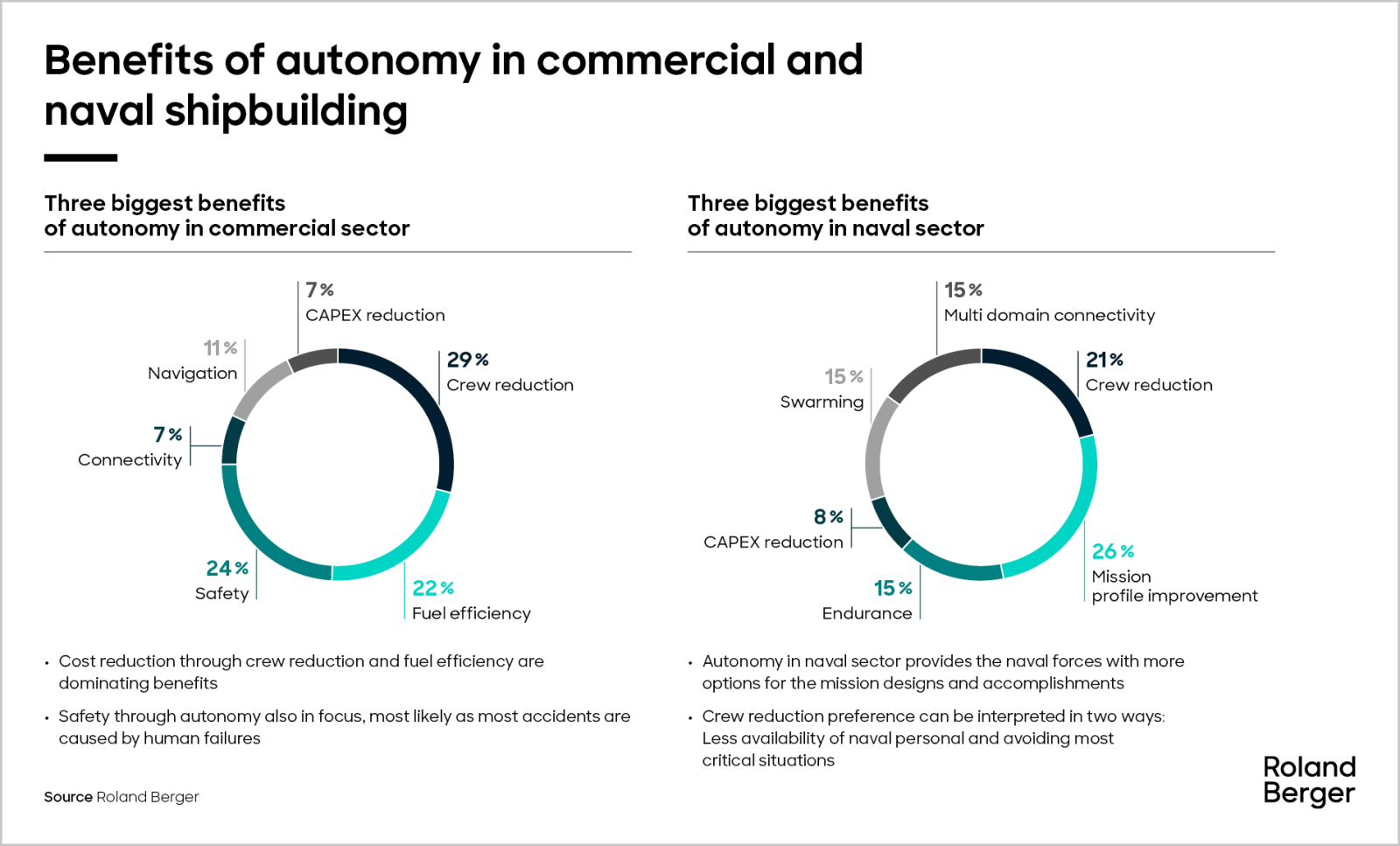

Commercial and naval priorities diverge

Commercial maritime operators focus primarily on operational cost reduction and efficiency improvements. The survey found that 29% of commercial respondents consider crew reductions to be the primary benefit of automation, followed closely by fuel efficiency optimization (22%) and enhanced safety protocols (24%), ahead of a number of smaller benefits.

"Europe and Asia are driving developments in autonomous shipping, accounting for 94% of industry leadership, while the focus in the Americas remains primarily military."

Military priorities differ. Here, the emphasis is on enhanced mission capability over cost reductions. Survey results show that mission profile improvement is the key military priority, cited by 26% of naval respondents, followed by crew reduction for dangerous missions (21%) and better operational endurance (15%). Similarly important are multi-domain connectivity (15%) and swarming capabilities (15%), with CAPEX optimization (8%) bringing up the rear.

Rather than considering the economic benefits, military interest in autonomous vessels centers on operational advantages. Uncrewed vessels enable extended missions, reduce personnel exposure to dangerous situations, and provide new tactical capabilities through coordinated vessel operations. On the commercial side, autonomous systems offer potential solutions to challenges around the shortage of skilled workers and rising personnel and operational costs, including fuel consumption, while simultaneously addressing safety concerns, given that human error is a contributing factor in three-quarters of all maritime accidents.

Barriers to autonomous shipping adoption

The slower-than-expected adoption of autonomous shipping technologies is a result of systemic barriers rather than technology limitations. Connected infrastructure represents the most significant challenge, according to 28% of industry professionals surveyed, followed closely by regulatory uncertainty (26%), with the International Maritime Organization (IMO) not expected to issue regulations for autonomous ships until 2030. Then there is the lack of technology standardization presenting a further barrier to market penetration, cited by 21% of respondents, alongside the availability of insurance (14%), navigation support (7%) and cost transparency (5%).

Economic impact expected to be substantial

Despite slower adoption rates, the industry remains confident of future operational savings. More than 60% of survey participants anticipate significant reductions in operational expenditure (OPEX) from autonomous shipping. Indeed, 38% of respondents expect OPEX savings to exceed five percent, while 23% predict between two and five percent lower costs. A further 15% anticipate modest savings of zero to two percent, and another 15% expect no change in OPEX. Only 8% of respondents believe autonomous systems will increase operating costs.

These optimistic projections stem primarily from anticipated reductions in crew costs and fuel efficiency improvements. Crew costs typically represent 30-40% of a vessel's operating costs, making personnel reductions a significant economic driver behind the adoption of autonomous and uncrewed ships.

Promising use cases and vessel types

The survey identified specific vessel types most suited to autonomous operation, revealing practical use cases where automation offers clear advantages. Passenger ferries and patrol/security vessels were each cited by 25% of respondents as the most promising use cases, while both cargo ships and offshore support vessels were mentioned by 20%. Tankers (7%) and private yachts (2%), on the other hand, are of limited interest for automation use cases.

Cargo shipping constitutes an ideal use case for autonomous technology due to its predictable routes, standardized operations, and significant potential for crew cost reductions. Container ships and bulk carriers operating on established trade routes could benefit substantially from being remotely operated.

Ferry operations offer the controlled environments suitable for automation, with fixed routes and established infrastructure. However, regulatory approval for autonomous passenger transportation remains uncertain and will likely require extensive safety validation.

Technology investment and R&D priorities

The industry's investments in R&D for automation focus on the core enabling technologies essential for autonomous vessel operations. Developing navigation software is the highest priority, being the investment focus of 30% of respondents, followed by sensors and camera systems (25%) and remote control technologies (20%). Lower down the priority list come port infrastructure (11%), personnel training programs (9%), and propulsion systems (5%).

Navigation software is the most critical technology, requiring sophisticated algorithms for collision avoidance, route optimization, and responding to the weather conditions. Current systems need to integrate multiple data sources including radar, lidar, GPS, and environmental sensors. Advances in sensor technology are driving the development of autonomous capability, with the industry investing heavily in computer vision, artificial intelligence, and machine learning systems. These technologies enable real-time environmental awareness and automated decision-making.

The survey revealed that the majority of companies (53%) are spending between five and ten percent of their total R&D budget on applications related to autonomous shipping. With 13% spending as little as zero to five percent, another 20% of firms are investing ten to twenty percent of their R&D budget in automation. Above that level are the 7% of companies spending up to half of their R&D budget on autonomous technologies and a further 7% assigning more than half of their research budget to automation.

Global market dynamics vary by region

Europe is considered the leading continent (56%) when it comes to the development of autonomous shipping, driven by favorable regulation and the environmental pressures. Asia is next (38%), exhibiting strong advances in technology and good manufacturing capacity. The Americas (6%) demonstrate limited activity, focusing primarily on military rather than commercial applications, while the Global South currently reveals no significant level of activity.

"We expect autonomous solutions to be standard shipping tools by 2040, but the route to get there will be a gradual one rather than a revolutionary change of tack."

Future market projections and expected timeline

The industry professionals offered insights into the expected adoption curves and market maturation for autonomous shipping applications. Looking toward 2035, 40% of survey respondents expect autonomous vessels to have captured zero to five percent of the commercial shipping market, while another 40% predict a five to ten percent market share. Taking a more optimistic view, 13% of respondents expect autonomous commercial vessels to account for ten to twenty percent of the market, while 7% even think they could constitute up to half of the market by 2035.

The outlook for 2040 is significantly more optimistic. By then, only 14% of respondents are expecting autonomous commercial vessels to account for zero to five percent of the market. The majority of responses are higher: 36% anticipate a five to ten percent market share, 29% expect ten to twenty percent, and 21% predict an even higher level of adoption, expecting autonomous commercial vessels to make up as much as half of the market.

These projections suggest gradual but substantial market penetration for autonomous technologies, with most growth expected to come between 2035 and 2040. This timeline aligns with the anticipated completion of the regulatory framework and the expected development of infrastructure and technology.

Measured evolution toward maritime automation

The study authors make a series of strategic recommendations for different industry stakeholder groups, from suppliers and shipbuilders to operators and regulators to maritime infrastructure providers and service companies, on the path to maritime automation. Further, the study highlights the potential advantages of dual-use products serving both commercial and military markets. Such applications may progress fastest due to reduced regulatory constraints in the military context, enabling faster technology validation and refinement.

The projected timeline of 2040 for widespread autonomous shipping adoption provides realistic expectations for industry transformation, allowing sufficient time for the regulatory framework to develop, infrastructure to be modernized, and technology to mature. This measured approach to maritime automation is more likely to ensure that robust safety protocols, comprehensive regulatory frameworks, and reliable technological standards are in place before the widespread adoption of fully autonomous shipping systems becomes reality.

Sign up for our newsletter

Further readings