Roland Berger is a thought leader in environmental issues and the response demanded from organizations. Our publications cover all relevant areas.

Green Gases: Perspectives from Europe and the US

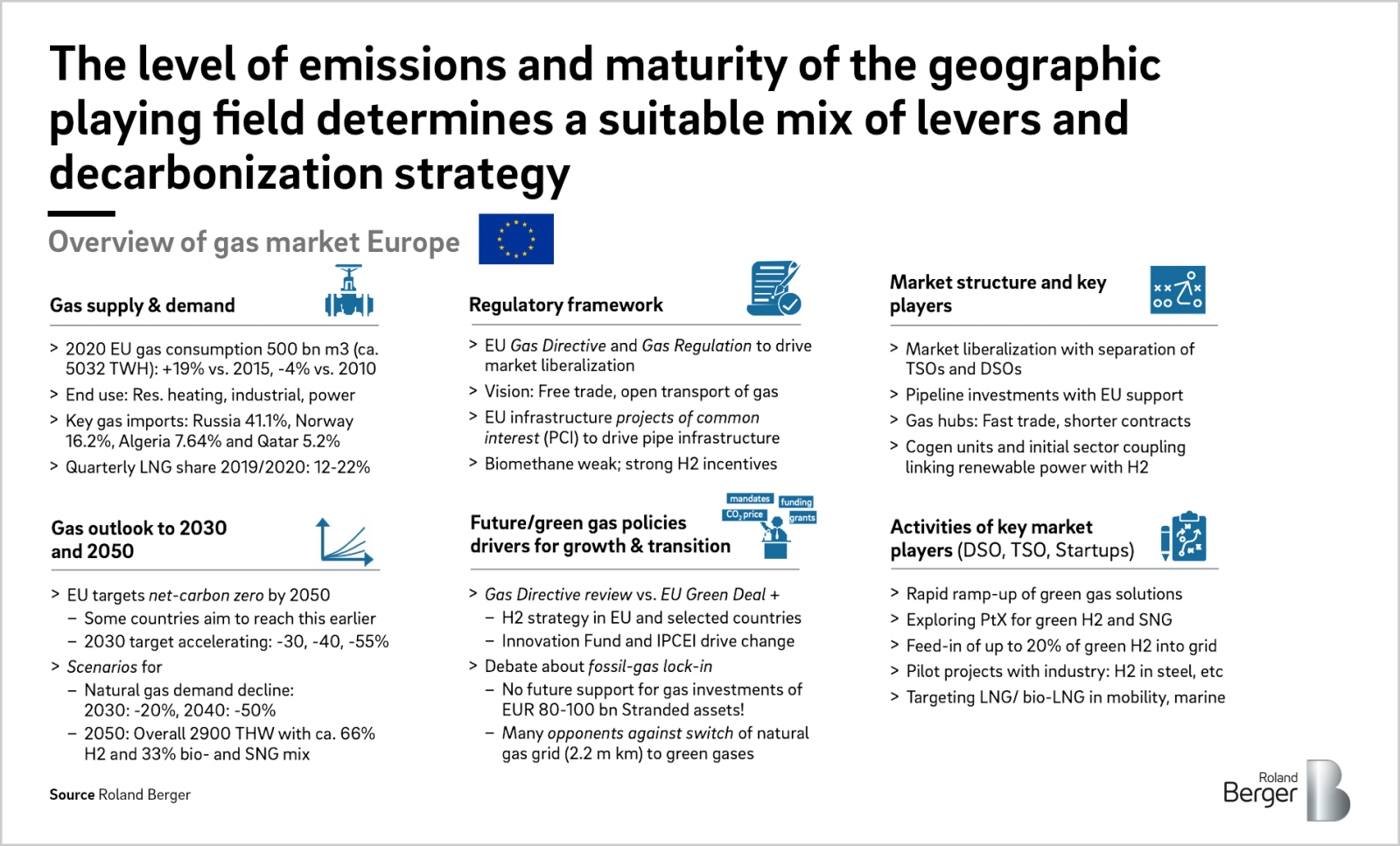

Comparing green gas policies and business models

The future of gas distribution networks is substantially affected by the emergence of green gases. Consequently, distribution system operators have to closely monitor the shift from natural gases towards green gases. Because this shift depends mainly on local factors, comparing different regions such as North America and Europe is important to track the latest developments and anticipate the newest trends.

To compare the two regions and encourage an exchange of knowledge and lessons learned, Roland Berger recently organized a Transatlantic Gas Exchange. At the inaugural meeting in June, 20 strategy executives from leading gas companies from the US, Europe and Latin America discussed the future of gas distribution networks. Keynote speakers presented perspectives on emerging strategies and programs in the US and Europe for production and delivery of low-carbon hydrogen and biogas (also known as renewable natural gas or RNG).

As part of the virtual meeting, participants engaged in a round robin of breakout discussions on the three key topics of green gases, government policy and business models. The discussions around these three fields revealed differences as well as similarities in the issues faced by gas utilities on either side of the Atlantic.

The North American perspective

While natural gas continues to play an important role in North America due to the economic advantages it brings, decarbonization policies and new business models have emerged as a potential threat to natural gases and create immense potential for green gases such as hydrogen and biogas.

However, technical issues around blending green gases such as hydrogen and biogas into US distribution network supplies need to be considered and watched carefully while initial demonstration projects are underway. One of the critical challenges is to ensure safety across the different customer segments. Another challenge that cannot be overstated is the resiliency of the energy supply . In February 2021, during the big freeze in Texas, the value of underground gas storage was very much appreciated. And the supply of green gases is a further challenge. Here, farmers are seen as key allies in obtaining biogas/RNG incentives, as this can significantly augment their income. In addition, technology and economic fundamentals point toward a major peaking, storage and backup role for low-carbon gas.

When it comes to policy, it is misleading to say that all of Europe is ahead of the US on gas decarbonization policy. Policies in some parts of the US (Northeast, West Coast) are more advanced than the policies in Eastern Europe, for example. On the other hand, in many conservative states US policy makers seem to be lagging significantly behind local market developments. As a result, it is difficult to enlist regulatory support for policies to promote new low-carbon sources . Distribution system operators (DSOs) are developing new partnerships with local governments, farms, universities and even private equity investors to support RNG. Regulators still do not recognize the value of today's natural gas infrastructure, and it is difficult for them to see the importance of gas networks in tomorrow's decarbonized energy systems. Intense energy demands in summer and winter peak periods are difficult and very expensive to supply with renewable electricity alone. 100% electrification of energy supplies would cost much more and deliver slower decarbonization results than a mixed solution involving green electricity and green gas.

In terms of business models for decarbonization , many investor-owned DSOs have created holding company structures to house both regulated and unregulated business (e.g. energy services, pipeline construction, perhaps hydrogen or biogas transmission/distribution in the future). DSOs intend to maintain a focus on "moving molecules" by pipe, which is their core business. There is not much near-term appetite for going into substantially different business models. Developing new or repurposed infrastructure for hydrogen delivery is a particular challenge for companies in regions with lower demands for heating or industrial energy. The demand and willingness to pay for green gases is currently limited to early adopters within the residential and corporate customer base but should broaden as costs come down.

The European perspective

European gas players are demonstrating exciting, integrated approaches to realizing the potential of green gases. Research and trials are underway to analyze the system and end use impacts of higher hydrogen mixes in pipeline gas. Many DSOs are focusing on facilitation of new biomethane supplies, as an initial step towards decarbonizing the networks. They are investing in technology adaptations to ensure that any blending of hydrogen into pipeline gas would work in the customer's appliances.

On the policy side, EU competition rules prohibit DSOs from providing anything other than gas transport services (i.e. pipes only). However, holding company structures can be used. Some DSOs are seeking approval for special tariffs or subsidies that incorporate development assistance and market access for decarbonized fuels. Many electric or combined electricity/gas utilities in Europe seem to be assuming that electricity will grow and natural gas will disappear. One key challenge is to demonstrate that while it may be technically possible to electrify a large portion of the energy demands currently served by gas, the same GHG abatement goals could be more quickly and affordably achieved through low-carbon molecular fuels. The focus is not only on decarbonizing the energy-carrying molecule but also on demonstrating the value of the current infrastructure. In addition, the infrastructure has value as a backup under multiple climate change/resilient scenarios.

Regarding business models, European DSOs are restricted at their level from engaging in non-distribution activities such as gas marketing or production, but related entities may do so. Providing decarbonization solutions to energy-intensive industrial customers (e.g. cement, steel, glass manufacturers) could be a role where DSOs can add value. European companies have had success in engaging directly with customers and partnering with oil and gas entities. On the customer side, similar to the US, the willingness to pay a reasonable price increment for green gas is not yet very common.

The international thought leaders who participated in the Transatlantic Gas Exchange all shared the common goal of finding ways for their companies to contribute their full capabilities towards achieving our shared climate change mitigation goals as quickly and affordably as possible, for the benefit of their customers in this and future generations.

Sign up for our newsletter

Sign up for our newsletter and get regular insights on newest publications related to Energy & Utilities.

Further readings

_tile_teaser_w425x260.jpg?v=1687234)