Polymer additive manufacturing – Market today and in the future

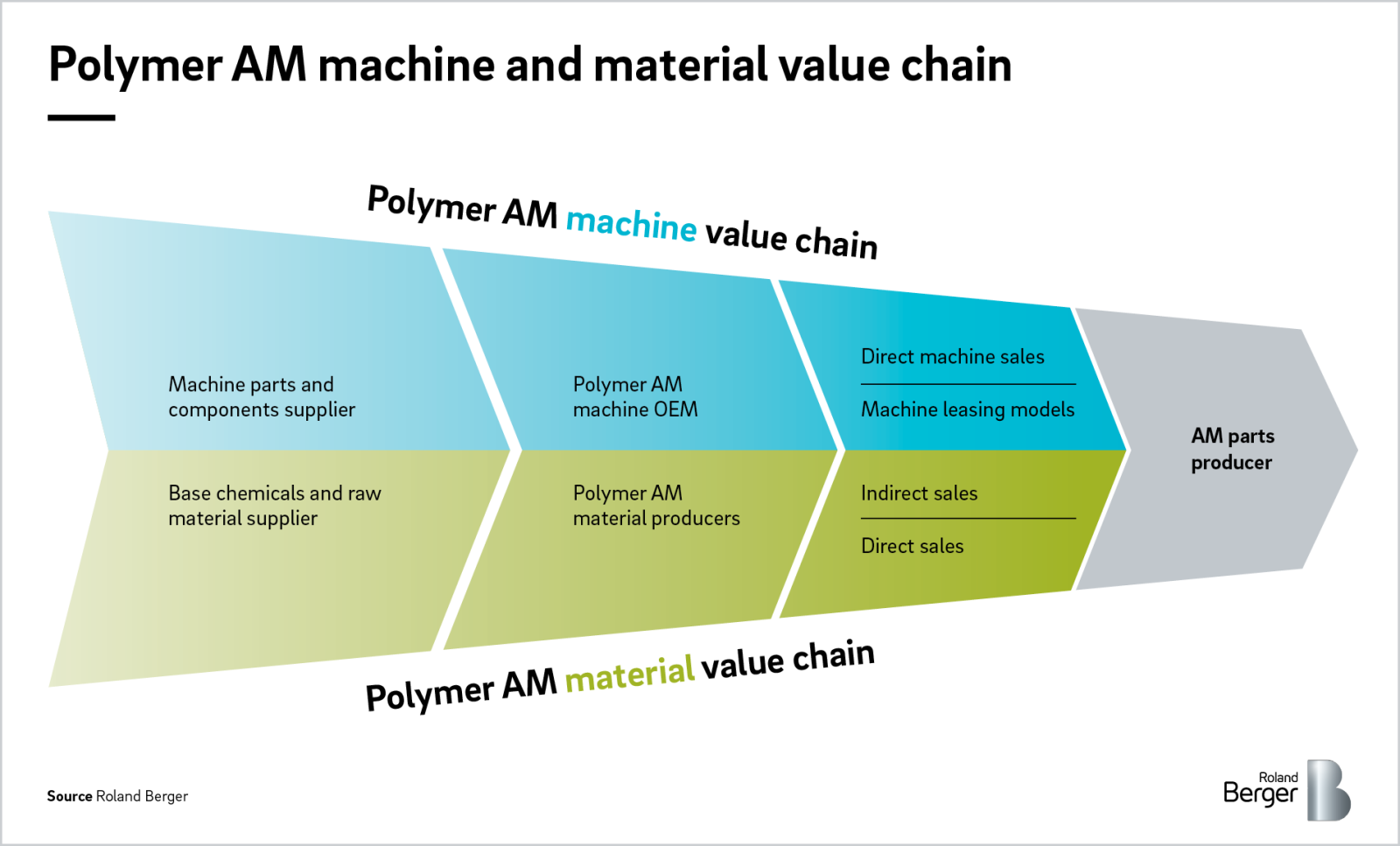

Market, machines and materials – The new playground for large chemical companies

In this study we take a close look at polymer additive manufacturing, an area that has attracted increasing attention since its commercial launch in 1987. This is the sixth in our series of studies on additive manufacturing (AM) , following on from our two papers on metal AM: Taking metal 3D printing to the next level and Advancements in metal 3D printing. In this paper, we examine the changes taking place in the polymer AM value chain and look at the latest market developments for machines and materials.

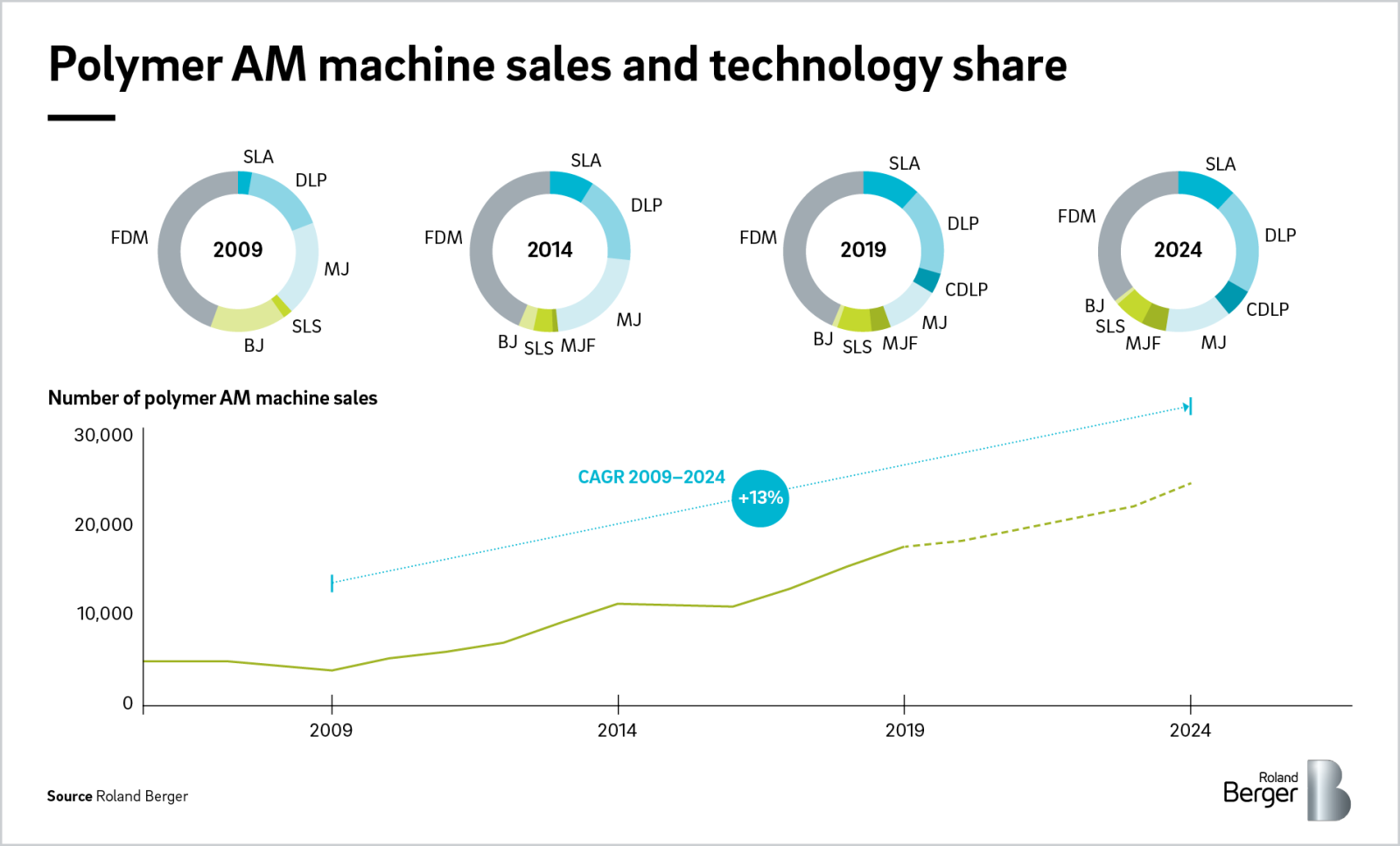

"Our bottom-up analysis shows that unit sales of professional polymer AM machines, which form the core of the market, are expected to grow by 13 percent from 2009 to 2024."

The polymer AM market is growing more complex with many different technologies, materials and players

Over the past two decades, the polymer AM market has seen major advances in user numbers, materials, systems and applications. More and more players are now entering the market, offering a diversified portfolio not only of materials and machines, but also of services and software. The number of serial polymer AM applications is rising, permanently changing some industries . For example, polymer AM enables the production of personalized hearing aids, dental mouth guards, prosthetics and orthotics, increasing patients' quality of life and improving medical outcomes. At the same time, printed consumer goods such as shoes, mascara brushes and shaving equipment show that customers are willing to pay for goods produced using the new technology.

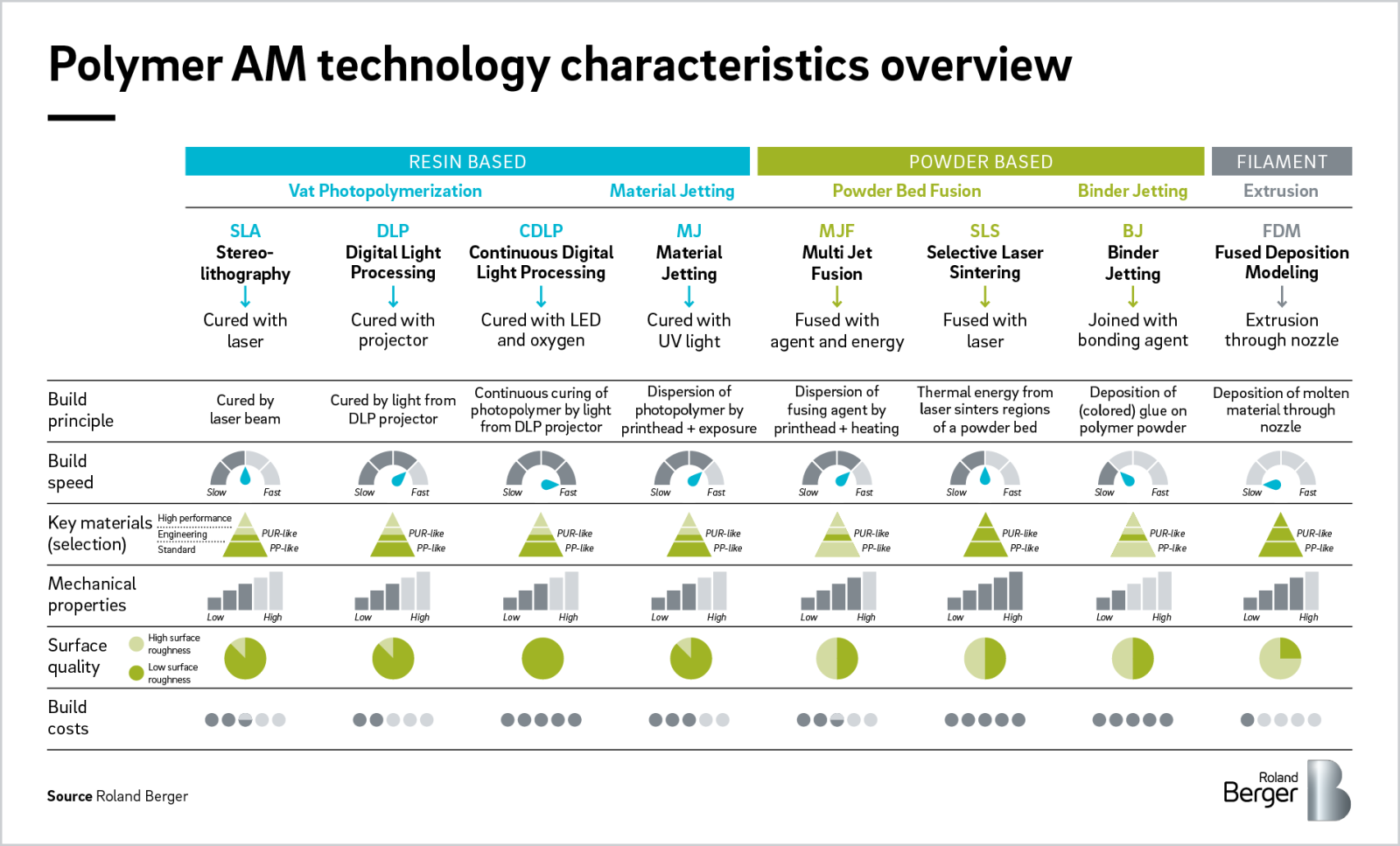

This willingness to pay, and the complex geometries of products that cannot be produced otherwise, are two of the key arguments justifying the high cost of polymer-based AM parts. Each application typically brings with it a unique set of requirements, and each of the eight polymer AM technologies currently found on the market has its own sweet spot. This makes it very likely that all eight technologies will continue to coexist in the future. The parts produced using different technologies differ in terms of their properties, such as their mechanical strength and surface quality, and therefore the build processes vary in terms of their speed and cost. The different technologies can also be categorized according to their position in the polymer material pyramid and whether the feed material is resin based, powder based or filament, as we explain below.

Each technology and material serves a portion of the market

The common material classes used for polymer AM are resin based, powder based and filament. Resin-based materials consist of epoxy or methacrylate groups and a photoinitiator, which together solidify when exposed to light or laser. Powders are controlled spherical-shaped granules such as polyamides (PA) of different chain lengths, thermoplastic polyurethane (TPU), polypropylene (PP) and poly-ether-ether-ketone/poly-etherketone-ketone (PEEK/PEKK), sintered together in SLS and MJF or "glued" together in BJ. Filaments are long, cylindrical polymers of different diameters that are reeled up on a spool. The range of materials offered is very broad, from polylactide acid (PLA) and acrylonitrile butadiene styrene (ABS) to polyethylenimine (PEI) and carbon fiber-filled filaments. Moreover, the range of such materials increases year on year in line with the needs of different customer applications. What has driven market growth in recent years? Machine sales growth is a leading factor. Professional machines sales – those costing EUR 5,000 or more – have experienced an annual growth rate of 13 percent since 2007.

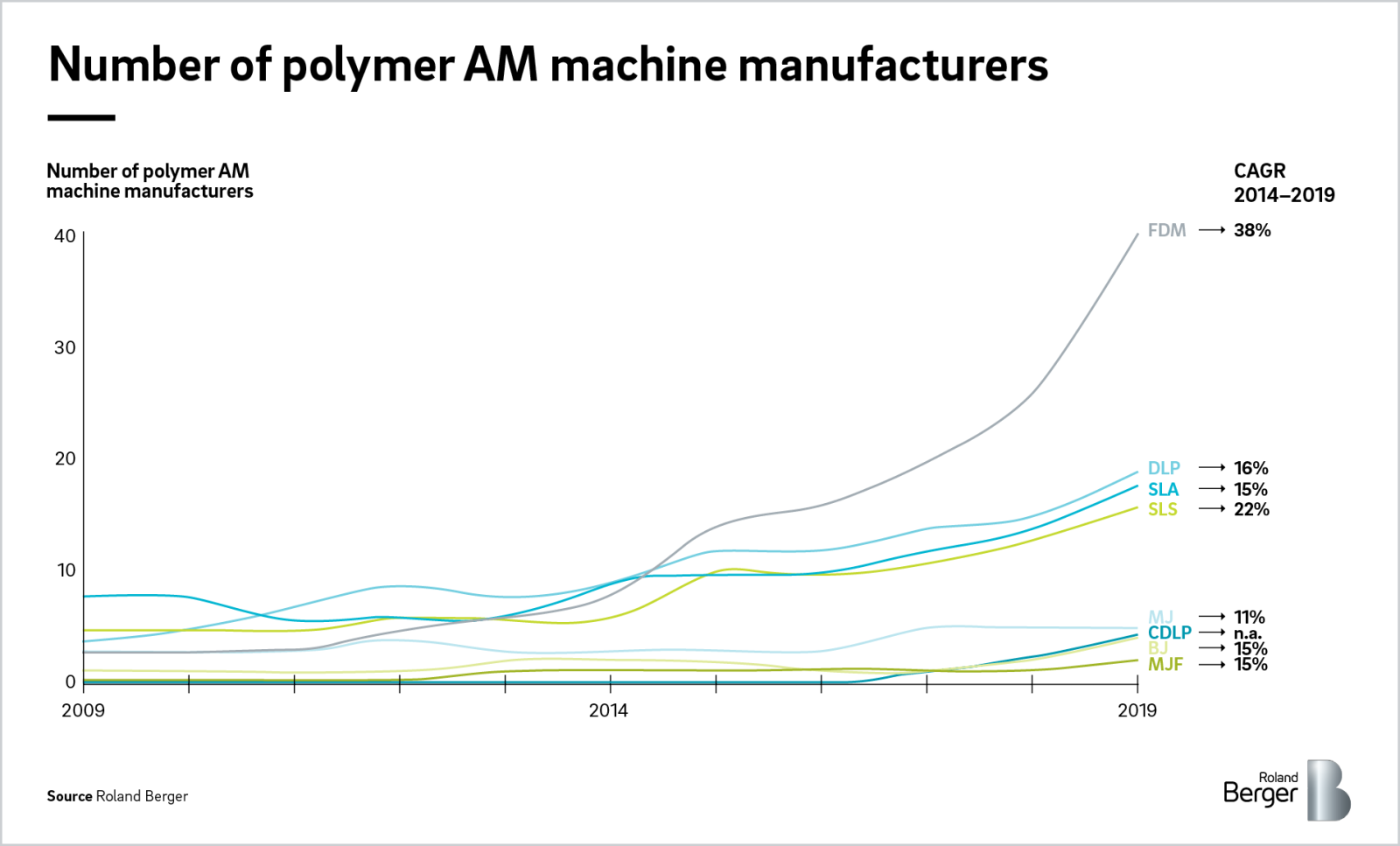

The size of the total market is a function of the installed base, machine utilization, print speed and development, and material. On this basis, we believe that double-digit market growth is reasonable. However, we do not expect to see growth rates of more than 30 percent. The share of each technology in the total market has been fairly stable to date, only disrupted by the introduction of CDLP and MJF. The main hurdles to a faster adoption rate are still the available materials, build speed and size, and the costs of parts and machines.

"Many machine OEMs have entered the market recently, a trend that we believe is set to continue. Overall competition will increase as the number of machine OEMs grows faster than machine sales."

Professional machine sales are expected to grow at a moderate pace

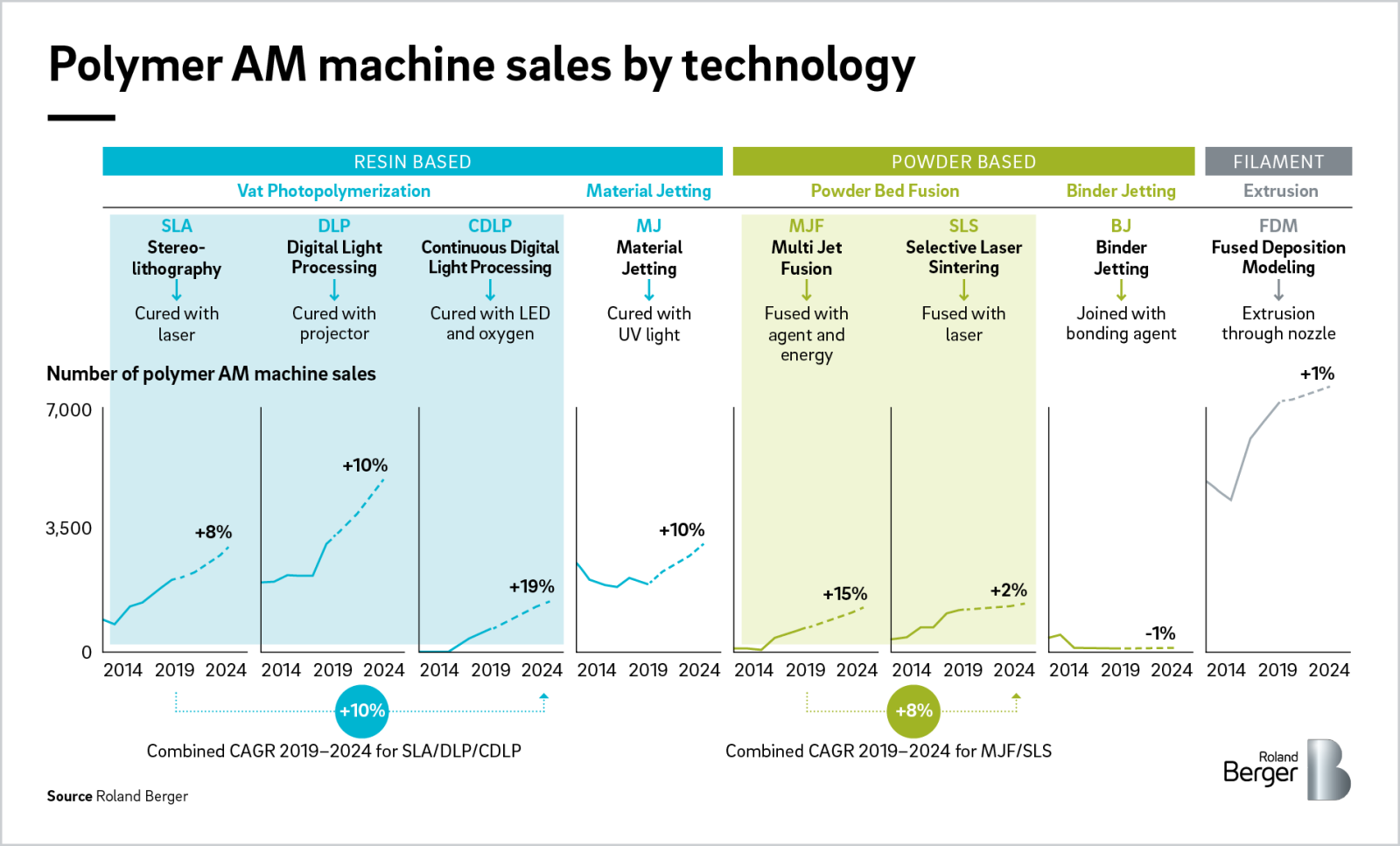

A detailed examination of machine sales reveals that although the machine market is growing overall, projected individual growth rates depend greatly on the technology in question. Thus, while CDLP is growing at the expense of DLP, and MJF is partially cannibalizing SLS, BJ is projected to become less important due to its disadvantages compared to the mechanical strength and color options offered by MJ and MJF. FDM benefits from cheap machines and materials, as well as the difficulty of making professional systems that cost over EUR 5,000 distinctive from cheaper desktop systems, and the significantly larger installed base. Nevertheless, continous carbon fiber FDM extrusion has attracted massive attention lately, as it also prints parts with huge dimensions. It is a technology in which a high-strength carbon fiber is extruded next to the common FDM filament to boost the mechanical strength in areas where the carbon fiber is placed.

We see co-existing technologies in the installed machine base today and in the future

Each machine in the installed base – estimated to be around 97,000 machines in 2019 – can only process a certain material class. Accordingly, materials are developed for specific machines, or vice versa. Some machine manufacturers offer "open" or "closed" machine systems to end users. With open systems, users can source their materials from third-party material suppliers; with closed systems, they can only use materials produced by the machine OEM. OEMs also protect their share of the market by means of patents on technological developments, such as light-induced sintering in MJF or the increased CDLP build speed principle.

Overall, we expect to see sales of vat photopolymerization systems (SLA, DLP and CDLP) grow by ten percent and powder bed fusion systems (MJF and SLS) grow by eight percent. Annual growth rates in the low teens will continue, we believe, as long as polymer AM is driven forward by advances in technology. The only factor that could potentially disrupt growth is if major serial applications led companies to invest in large-scale printing farms and accelerated growth.

Despite these moderate growth rates, the machine market remains interesting for many companies. Since 2014, we have seen a dramatic increase in the number of machine OEMs offering professional systems. Growth has been particularly strong for cheaper systems (FDM and DLP) and technologies for which patent protection has expired. Looking ahead, we expect to see the number of machine OEMs grow faster than sales of machines, leading to increased competition.

"Large chemical companies are entering the polymer material market, attracted by the promise of market growth and high margins. New entrants need a solid strategic approach."

We expect intense competition in the machine OEM market

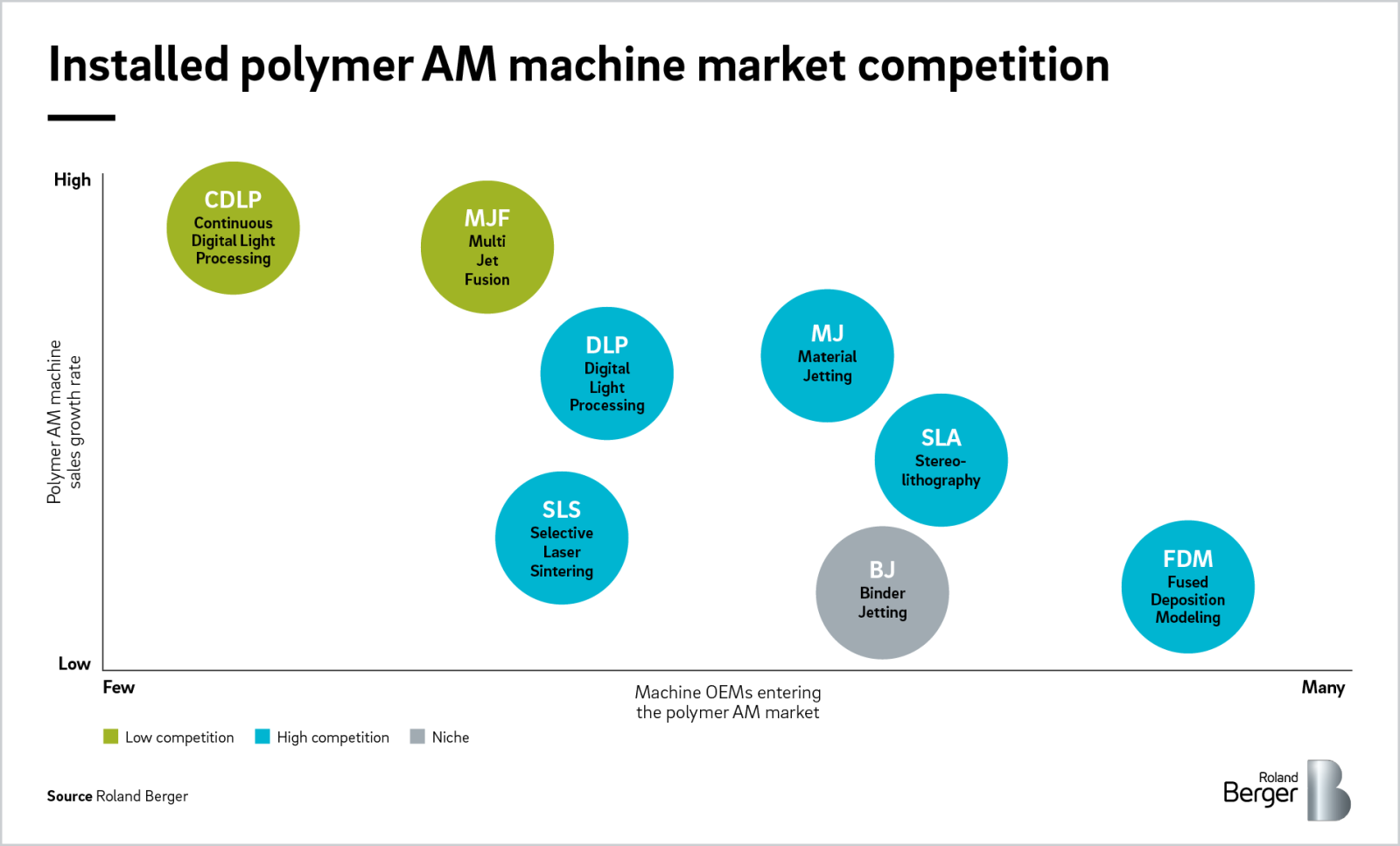

Using the information currently available and our market forecasts, we are now in a position to draw up a competition matrix for the polymer AM market. We find that CDLP and MJF are likely to face little competition, as their technology is protected by patents. BJ is a niche technology, with fewer manufacturers and decreasing sales. In all other technologies, we expect to see competition increasing. In response, machine OEMs can already be observed changing their business models to printing services, maintenance business, consulting, pay-per-part and hardware-as-a-service. Materials and machines are closely linked in polymer AM. This means that it is easier to protect closed systems, and we are likely to see machine OEMs with such systems adding material sales to their revenue sources and trying to protect this business. Unlike with metal AM systems, closed systems will continue to dominate the market for resin-based materials. Some user environments also favor closed systems as a way to ensure quality, usability and fail safety, for example in dental clinics. For open systems, filaments and powders already face stiff competition. With more and more machine OEMs also offering materials and open systems, the range of available materials has increased significantly – a development that has put material prices under pressure.

Like the machine manufacturer market, the polymer material market has seen major changes in recent years. Noticeably, more and more large chemical companies have developed their own 3D printing material, as revealed by the number of such companies now present in the market. In the chase for high margins and high growth rates, some companies have made major investments in acquisitions , material R&D and marketing. For example, DSM and Evonik were early adopters in the material market. Huntsman and Dow/DuPont have even been producing AM machines besides offering materials despite having quit the machine sector years ago.

Chemical companies have entered the polymer AM material business to grab a share of the market

With many new players hoping to capture a share of the polymer AM material market, it has become increasingly important to understand the key success factors for suppliers. Three main strategic factors stand out in our examination:

- Distinctive value proposition

Companies entering the polymer AM material market must offer customers products based on their specific polymer printing segment. Players such as Evonik with PA12, Sabic with Ultem™ and DSM with Somos® show that chemical companies can establish brands with strong recognition in the market . The range of materials available on the market is expanding continuously, and it is essential that end customers know which material is best for the application in question. Companies should ensure customer retention at an early development stage through lighthouse projects and partnerships. This is particularly challenging for closed systems, as it requires close cooperation with end customers and machine OEMs at the same time. - Clearly defined position in the value chain

With eight polymer-based AM technologies and around 100 machine OEMs, the polymer AM market is nothing if not complex. Covering multiple parts of the AM value chain brings additional complexity. Selecting the right part or parts of the value chain in which to operate is essential if companies wish to enter the market successfully, create a dominant market position and defend their market share against competitors. A clear strategy roadmap can be of critical importance, not only as a basis for customer interactions and defining the scope of the material portfolio, but also as the foundation for decisions about organic or inorganic growth. - Robust partnerships with machine OEMs

Players need strong partnerships with machine OEMs in order to enter the market and then defend their market position. In the case of closed systems, this is crucial. In open systems, such as FDM and SLS, competition is increasing and it will be hard for established players such as Evonik and Arkema to defend their market position, price level and resulting EBIT margins. Working closely with machine OEMs and end customers to guide applications from the lab through to serial production will drive success and prevent cheaper materials flooding the market.