Think:Act Edition

Rethinking Growth

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/Cover_Image_EN_download_preview.jpg)

Think:Act looks at smart growth, from efficiency and ideal group size to dark tourism, sports technology innovation at FC Barcelona and the data gender gap.

Published April 2020. Available in

by Bennett Voyles

illustrations by Serge Bloch

photos by Ragnar Schmuck

A new decade is swinging open its door – and behind it lie some difficult questions for business. Have we outgrown growth? Is it still good? And how can a company navigate an era that could turn established economic thinking on its head?

Ready or not, the twenties are here, and they're looking ugly. Global warming, trade wars, aging populations, wealth disparities, automation-induced unemployment, unmanageable sovereign debt and the challenge of building – and paying for – digital transformation could all stunt corporate growth. To make matters worse, analysts at the United Nations Conference on Trade and Development warn that most governments are unprepared for any sort of macroeconomic shock. "A spluttering North, a general slowdown in the South and rising levels of debt everywhere are hanging ominously over the global economy; these, combined with increased market volatility, a fractured multilateral system and mounting uncertainty, are framing the immediate policy challenge," they wrote in their annual report in October 2019.

Grim as all that may sound, some business thinkers argue that the next decade may also be a time of opportunity for at least a few companies. They say companies that learn to focus less on raw growth and more on keeping their customers happy, their employees engaged and creative and their processes sustainable may be resilient enough to survive any number of challenges and nimble enough to take advantage of any opportunities that do present themselves. "Recessions aren't always uniformly bad for all players – many of the world's most successful businesses were born in recessionary times," says innovation expert Rita Gunther McGrath , author of Seeing Around Corners: How to Spot Inflection Points in Business Before They Happen and management professor at Columbia Business School.

"For companies that have husbanded their resources, recessions can be a good time to selectively expand their capabilities," she adds. "Good people become more available. Lots of assets, such as desk chairs, get given away for pretty much nothing. Small firms that struggle to stay afloat or to raise additional funding become available for acquisition or 'aqui-hire.' Some overstretched firms will pull back from markets and leave them to the competition."

So how should you set your company up to thrive through the bumpy ride? While the fundamentals still apply – watch your margins, keep your working capital lean, stay close to your customers – some business thinkers suggest additional measures as well.

The first item on a lot of advice lists is to make sure your financial goals align with your stated goals. In August 2019, for example, the Business Roundtable, a group of nearly 200 CEOs of US corporations, agreed the purpose of the corporation included delivering value to customers, investing in employees, dealing fairly and ethically with suppliers and supporting their communities. Generating long-term value for shareholders was the fifth and last item on the list.

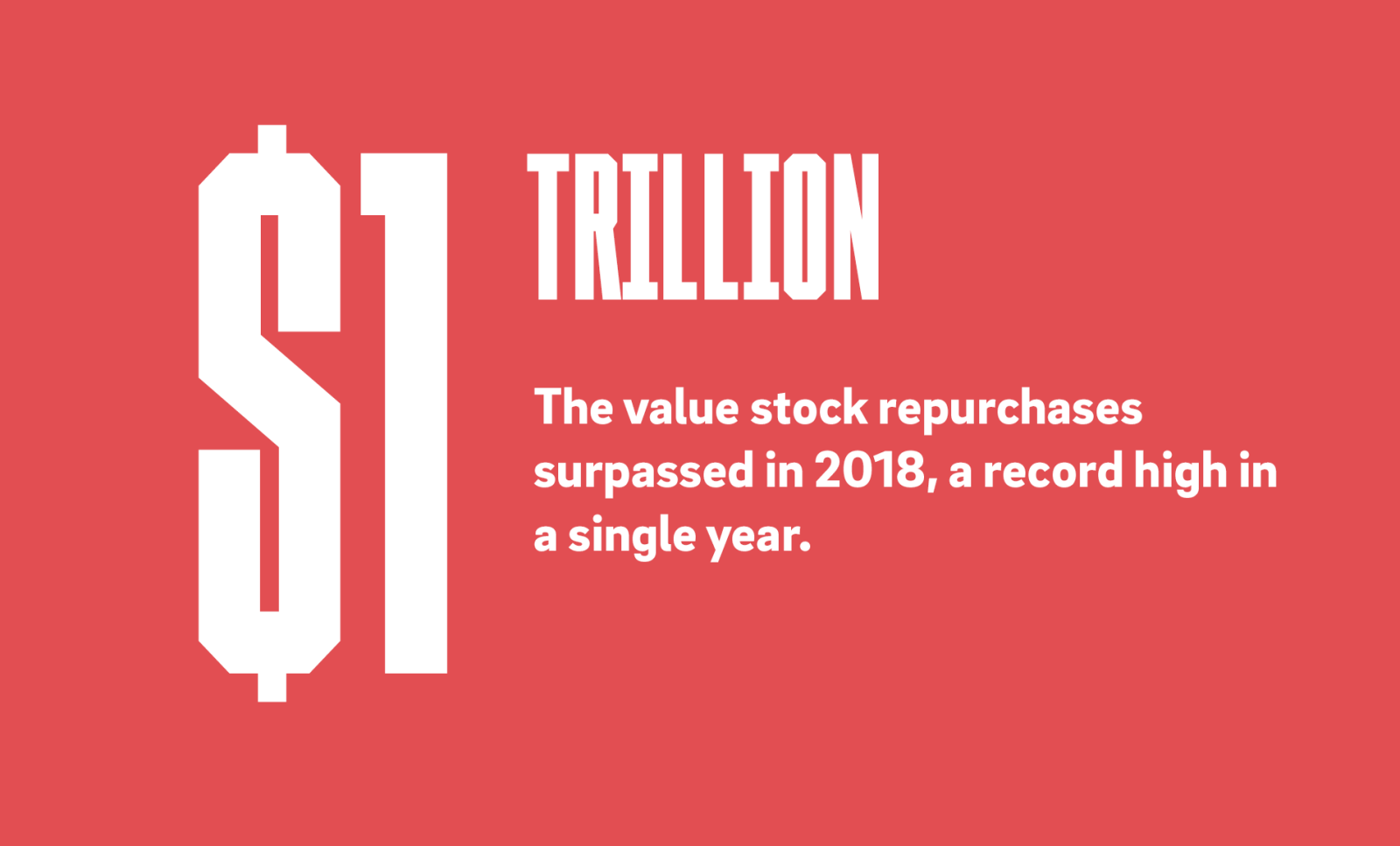

Although big business may have emotionally left the maximization of shareholder value era, structurally, Milton Friedman's free-market capitalism is alive and well: Many CEOs still receive a lot of their compensation in stock, giving them an added incentive to try to keep their share price high, and they have a handy fan that helps to keep it aloft – the stock repurchase. It's been 10 years since Jack Welch, former CEO of GE, told a shocked Financial Times reporter that maximizing shareholder value was "the dumbest idea in the world," but share buybacks are now more popular as ever, with a total value that topped $1 trillion in 2018.

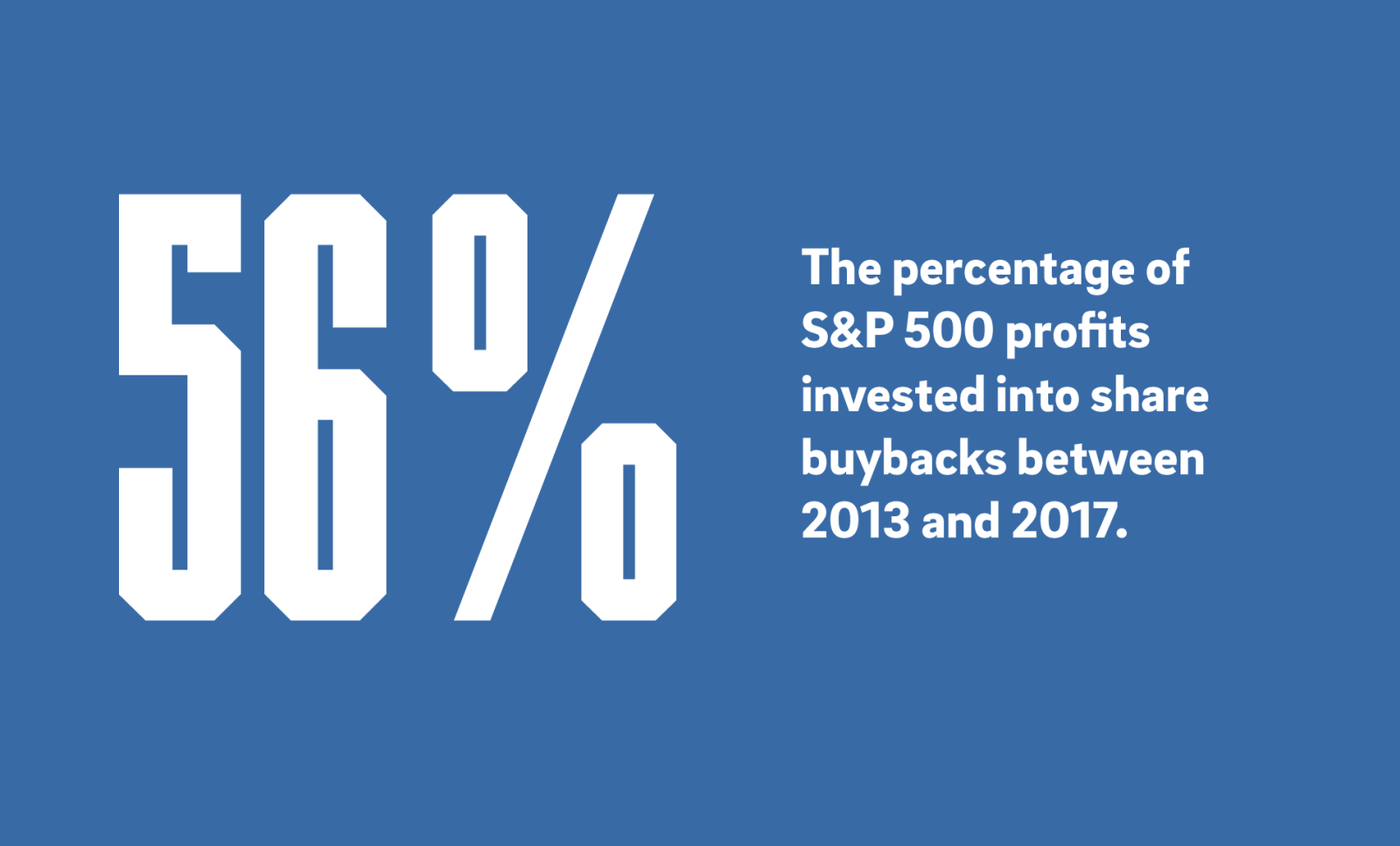

Before the 1982 decision by the Securities and Exchange Commission to liberalize rules about share buybacks, companies invested a lot of their income in innovation and enhancing the skills of their employees. That changed dramatically in the three decades that followed: Between 2013 and 2017 alone, S&P 500 firms invested $2.6 trillion – 56% of their profits – in share buybacks, according to a presentation by William Lazonick, a professor of economics at the University of Massachusetts Lowell. Buybacks might be seen as a victimless shift of cash from one pocket to another, but Lazonick has long argued that buyback programs enrich executives at the expense of their companies, sucking resources away from research and Development and employee training.

McGrath agrees: "The irony is that the very policies that are supposed to be helpful to shareholders actually have the effect of harming the long-term performance of businesses whose leadership essentially uses the capabilities built up over years to make themselves unbelievably rich, among other things. Many companies today are very much out of balance between running today's business and investing for the future – the latest poster child would be GE, which issued massive buybacks during [Jeffrey] Immelt's era but didn't lean into renewable energy investments at the level they could have. But you could see the same story at many other firms – Kraft Heinz and Sears, for instance," she adds. Meanwhile William Fischer, a professor of innovation management at IMD in Lausanne, says that buybacks are always a sign of managers with insufficient imagination. "I think they're probably caught between some big changes that are difficult to understand...and shareholders who are pushing for quick returns," he says.

Another defensive strategy some experts suggest is to find partners who will work with you to serve your customer in ways that go beyond your traditional boundaries. Chinese appliance giant Haier, for example, is beginning to focus less on manufacturing individual products and more on working with a variety of partners to develop larger cross-company ecosystems that better serve customer needs, through such initiatives as its Internet of Clothing project, according to Fischer, an advisor for the company. The Internet of Clothing consortium takes washing machines and driers as a starting point for a whole constellation of clothing-related initiatives, including even specialized detergent companies. Such collaboration can help serve the customer better while reducing the partners' risk of bringing a technology to market that customers don't want. "By creating ecosystems where you have a whole bunch of firms that have loose connections to one another, you increase the likelihood that at the end of the day, you'll go to market with not only an idea that's interesting, but also the supporting infrastructure to make the idea easily adoptable," he explains.

To make these ecosystems even more robust, Haier organizes them in a way that discourages squabbles by working out in advance not only the partners' relative contributions to the product or service, but also the relative share of revenue they will take out of it, according to Fischer.

Steve Blank, a Silicon Valley entrepreneur whose work paved the way for the lean startup movement, is also positive about the potential of companies to win by expanding their innovation ecosystem. "Startups, since they're so well funded, now have as much or more cash and R&D dollars than the companies they're dealing with, and that's a big idea. If you're inside a company and you can now concatenate the resources of 10, 20, 50 of these startups that are incredibly well funded, and those R&D dollars don't show up on your books, they're on the VC's books, but you can get the output of that for licensing, that's a source multiplier," he adds.

Fischer's advice is also to look beyond the company's traditional boundaries. He adds: "Traditionally, disruptive innovation almost always comes from outside, from the edge, not from within the cohort of successful market-leading incumbents, who are benchmarking against each other and doing pretty much the same thing in the same way," Fischer advocates expanding your horizons, perhaps paradoxically, by reorganizing into smaller units. Here Fischer also sees a model in Haier, which has reorganized much of the company into tiny teams of 10 or fewer people, all with semi-independent missions.

"They're sort of reversing the direction of the typical growth engine and trying to move away from being a large, inflexible firm into a smaller, more nimble set of firms, albeit with a big brand and access to resources that small firms don't have."

Professor of Business Administration and the first Batten Executive-in-Residence at the University of Virginia Darden School of Business Edward D. Hess argues that the only kind of growth worth pursuing is the kind that helps everyone affected by the business. "Smart growth creates positive value for all stakeholders, including workers and society," explains Hess, who is also the author of Smart Growth: Building an Enduring Business by Managing the Risks of Growth. Dangerous growth occurs "when the organization is making irrational investments or when the organization is diversifying into an area where it lacks competence and has no rational plan to manage the risk," or is too complacent, and "keeps doing what has worked before in spite of data that clearly shows the market has changed or new products or services are needed by customers."

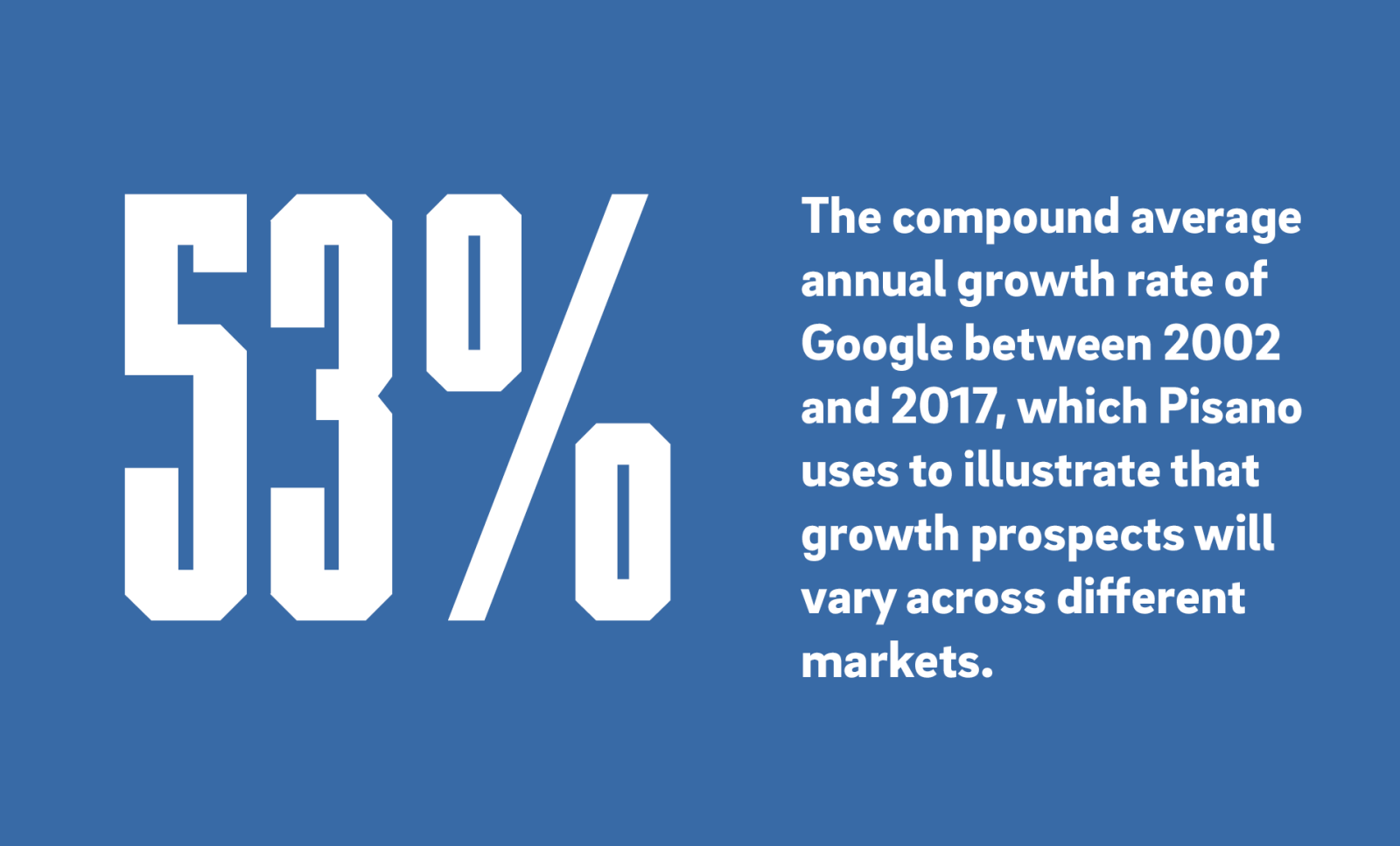

As attractive as fast growth might seem to be for investors and employees, it often doesn't end well. In a recent empirical analysis of 2,500 US manufacturers' long-term growth between 1959 and 2015, Gary Pisano, the Harry E. Figgie, Jr. professor of business administration at Harvard Business School, and his three co-authors found that few firms grow steadily for long, and those that do tend to belong to fast-growing industries.

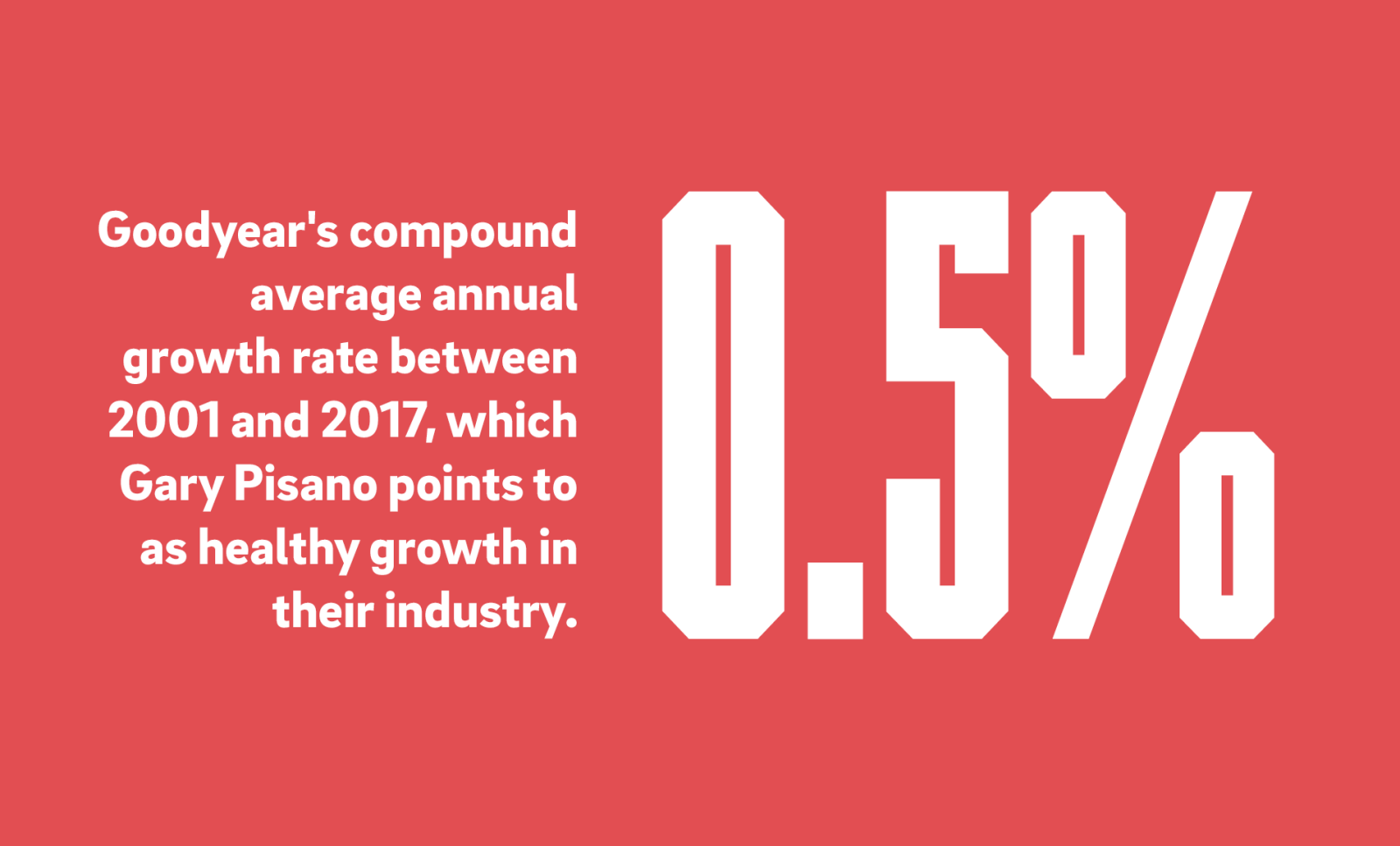

As Pisano recently told Harvard Business School Working Knowledge, companies often have unrealistic expectations. "The data suggests that companies should be more realistic about their growth rates, not expecting rapid growth year after year," he says. Even those few that do grow well for a long time often fall apart suddenly in the end. Pisano points to the 1990s and the sudden decline of Digital Equipment Corp. "Sometimes a controlled growth rate is healthier in the long run, "Pisano notes. "Even though investors may want to see higher growth, it may be better to sacrifice some short-term growth to gain persistence."

Jerome Barthelemy, professor of management at ESSEC Business School and author of Tout ce que vous savez sur le management est faux (Everything You Know About Management Is Wrong), warns against growth for growth's sake. Barthelemy likes to quote Southwest Airlines founder Herb Kelleher: "I would rather have 4% of the market and be profitable than 24% of the market and lose money." Barthelemy says where companies go wrong is that "those who aim for growth often reverse cause and effect. While success leads to growth, growth does not necessarily lead to success."

Making a reference to British economist John Kay's 2010 book Obliquity: Why Our Goals are Best Achieved Indirectly, Barthelemy points out that the fastest-growing companies tend not to pursue that growth directly. Often, Barthelemy says, growth is like happiness – you can't really achieve it through direct pursuit. "Growth is something that comes out of a robust strategy and it will come naturally. If you focus on growth per se, then you can get into trouble," he says, noting that corporate crashes tend to be divided almost equally between companies that failed because they grew too slowly and companies that died because they grew too quickly.

At Acceleration Partners, a young affiliate marketing company with more than 150 employees headquartered in Needham, Massachusetts, CEO Robert Glazer saw many peer companies taking outside risks to grow. That’s when he decided that if he made Acceleration Partners a great place to work, the company would attract great people, who would in turn raise the company's level of performance.

In order to support that strategy, he changed the stated corporate values in a way that also focused on commitment to work rather than the results. Instead of just asking for accountability, he wanted employees to "own it," he said, by which he meant not only that individuals should be accountable for a project, but that they take complete charge of it. Instead of the passivity that can creep into traditional corporate work – I did my part; too bad the project failed – he wanted to see employees who were "owning it," who felt they had an entrepreneurial stake in the outcome.

Indeed, this proved to be a difficult shift at first. "It's harder for people to grab on to things that are more qualitative than 'we want to get to X million in revenue,'" Glazer said. But just two years later, Acceleration Partners has won a number of awards from Glassdoor and other company evaluation firms as a great employer. The company is still growing, but when Glazer and his team make decisions now "it's through a long-term lens...it's not, 'how fast can we drive the bus for the next three months?' as a lot of our industry does. We want our mantra to be: The journey is the destination."

Think:Act looks at smart growth, from efficiency and ideal group size to dark tourism, sports technology innovation at FC Barcelona and the data gender gap.

Curious about the contents of our newest Think:Act magazine? Receive your very own copy by signing up now! Subscribe here to receive our Think:Act magazine and the latest news from Roland Berger.