How retail can protect its future

Study

Quick commerce – a lasting revolution?

![{[downloads[language].preview]}](https://www.rolandberger.com/publications/publication_image/roland_berger_ins_948_quick_commerce_cover_download_preview.jpg)

How omnichannel retailers are rising to the challenges of q-commerce

Published December 2022. Available in

Quick commerce or "q-commerce" – online shopping with a delivery time of under 30 minutes – is causing a revolution in retail. Will its impact on the industry be permanent, and how should omnichannel retailers be responding? Can they find a way to make q-commerce profitable while still providing the convenience that customers demand in terms of speed, price, product availability and so on? To understand the changes taking place in the market, we surveyed more than 6,000 consumers in Germany, France and the United Kingdom. Using this data and analyses of the retail landscape, we investigate the potential of q-commerce and look at how omnichannel retailers can rise to the challenge.

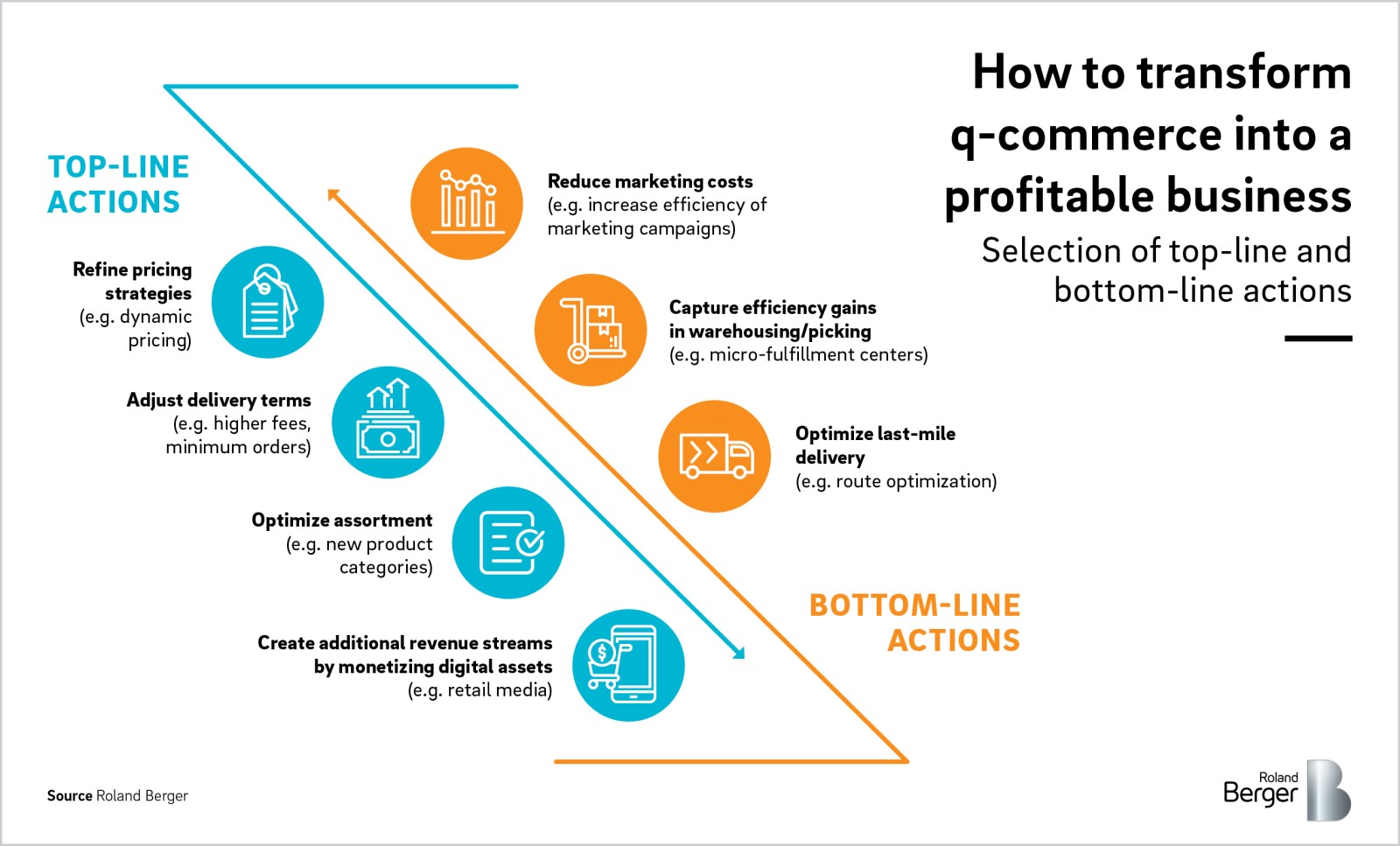

"Only the most efficient players – those who keep their costs low and become profitable – will survive the coming market consolidation."

At first sight, q-commerce looks like simply a step-up in service levels – a natural progression from same-delivery to maximum 30-minute delivery times. But, in fact, we believe that it represents a completely new convenience channel, with its own unique business model. What sets it apart from "traditional" e-commerce is that it mainly targets spontaneous, emergency and emotional purchases by consumers. What is more, it competes not only with traditional online but also with stationary convenience retail formats, such as corner shops and minimarkets.

The q-commerce market initially focused primarily on groceries and meal deliveries. Now, players have started expanding into other retail categories, for example, offering a cross-category assortment made up of fashion, beauty and home decoration items. The size of the potential market means that retailers would be wrong to ignore it. For example, if around 12 percent of the EUR 730 billion groceries market in the United Kingdom, France and Germany move online by 2030 and q-commerce accounts for just 15 percent of online orders, the market will be worth EUR 13 billion. And if q-commerce expands to include more online product categories than today, this would mean a sizeable additional increase in market size. The critical question, however, is whether the revenues from product margins, commission fees, customer delivery fees, service fees and in-app advertisements can cover operating costs and make the business model lucrative. The answer to that question is unclear at present: Product prices in q-commerce are similar to those in the supermarket, marketing for brand-building can account for up to 30 percent of total costs in the initial phase, and delivery fees rarely cover the actual costs.

Our survey of consumers produced three major findings:

Multichannel retailers wishing to expand into q-commerce have two main options: They can partner with an existing q-commerce provider, or they can build their own q-commerce operations. The partnership model has many advantages and we believe it will be the preferred strategy for most multichannel retailers. Thus, platforms are highly attractive for customers, they encourage customer loyalty and they have good customer reach. The partnering option also saves retailers the large initial CAPEX investment needed to launch your own operations. The second option is to build your own q-commerce capability. This entails a massive initial outlay for the q-commerce platform, inventory and warehouse logistics. On the plus side, however, it means that you stay in charge of the vital consumer interface, retain margins and can exploit your existing store network.

Whether q-commerce finds a permanent place for itself in the retail landscape or not, omnichannel retailers need to engage with it as a matter of priority, adjusting their channel strategy in line with this new understanding of convenience. Some players will choose to cooperate with existing platforms, while others will build their own q-commerce delivery services. In both cases, a key challenge will be how to integrate q-commerce into an omnichannel offering without cannibalizing other channels – especially traditional bricks-and-mortar stores.

How omnichannel retailers are rising to the challenges of q-commerce