The COVID-19 pandemic will hit the economy harder than the 2008 financial crisis, and most industries will recover slower this time than they did after the financial crash.

World economic growth plunges due to coronavirus - which industries are suffering the most

Our corona economic impact series - Part 2

Global Topic

Macro Analysis

Corona Economic Impact - Part 1

Corona Economic Impact - Part 3

Around 170 countries now have confirmed cases of COVID-19. Inside China the number of new infections has rapidly slowed down, but there are major outbreaks in Italy, the United States, Spain, Germany and Iran. New infections in Europe and the United States are likely to increase exponentially over the coming weeks, while clinical trials and approval processes for the antiviral drugs and vaccinations currently in development may take several months yet.

In our previous update we outlined three scenarios for how COVID-19 will affect different countries and industries. Our most optimistic scenario – "Fast Recovery" – no longer appears realistic. In this update we focus on our second scenario, "Delayed Cure". We break this scenario down into two sub-scenarios, one in which the current economic disruption continues for four weeks, and one in which it continues for twelve weeks.

Global roundup

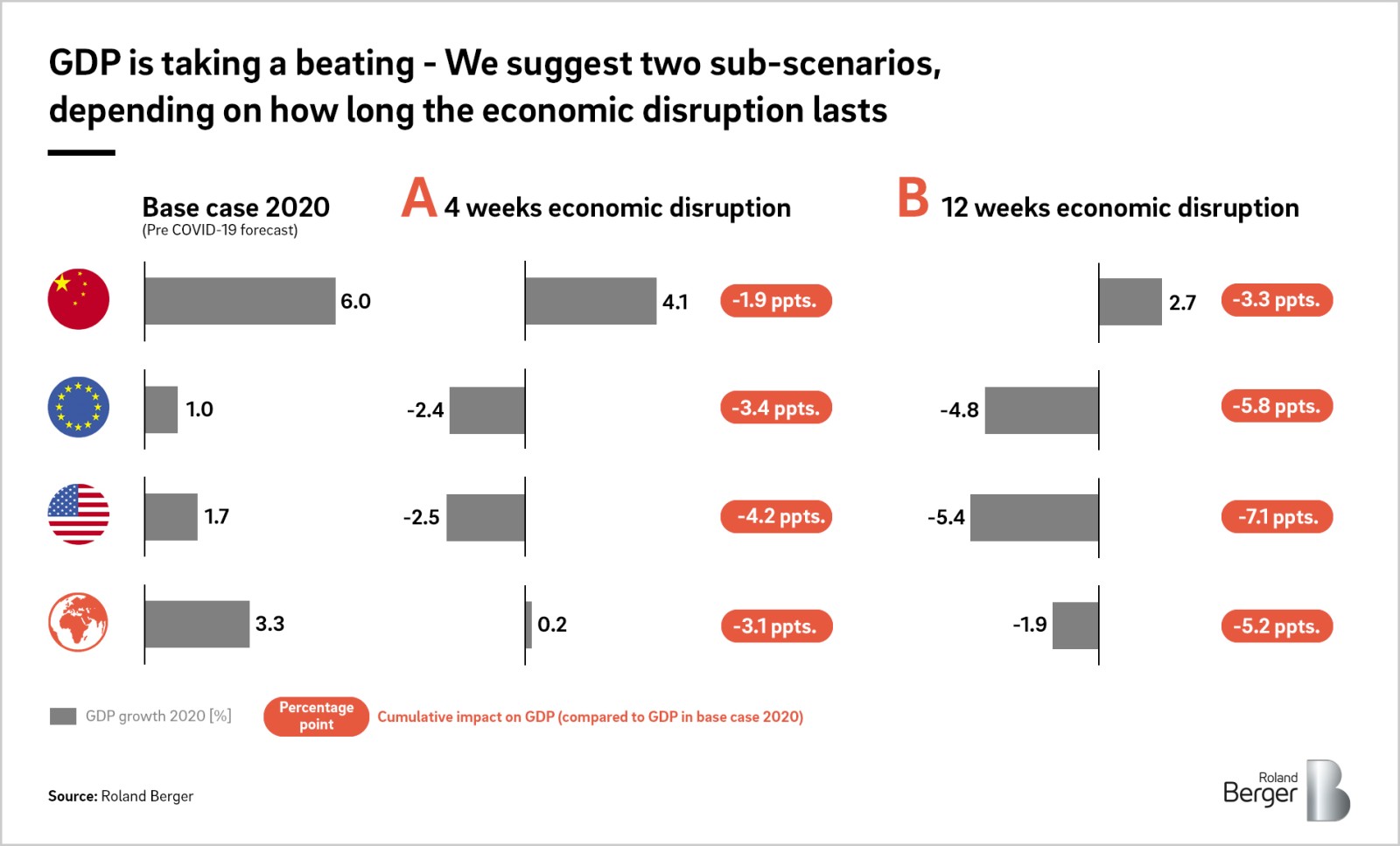

One thing is clear: GDP is currently taking a severe beating. However, the size of the impact in different parts of the world will depend fundamentally on how long the present economic disruption lasts. We foresee a drop in GDP growth in 2020 compared to the pre-crisis base case ranging from 1.9 to 7.1 percentage points.

China is further along the coronavirus curve than Europe and the United States. The government's actions have been effective, quarantine measures have been gradually lifted and social and economic life is slowly returning to normal. In the event of a four-week economic disruption, China will feel the effect of closures of production sites and lack of demand from the United States and Europe, but production will quickly return to normal driven by pent-up domestic demand and demand from key trading partners post-lockdown (Japan, South Korea). The result will be a drop in GDP growth of just 1.9 percentage points in 2020 compared to the pre-crisis base case. In the event of a 12-week economic disruption, European and US demand will remain in the doldrums for longer and domestic demand will not completely compensate for this, leading to a drop in GDP growth of 3.3 percentage points.

If mitigation actions by governments in Europe are effective, we could see the number of new infections declining here at the beginning of Q2 2020. A four-week period of economic disruption will mean negative growth in Q1 and Q2, i.e. we will have a recession and GDP growth for the whole of 2020 will be down 3.4 percentage points. Should the disruption continue for 12 weeks, on the other hand, we foresee a steep drop in growth in Q2 2020, with the closure of many non-essential production sites and a substantial increase in unemployment, especially in the services sector. In this case GDP growth for the year could be hit by as much as 5.8 percentage points.

Four weeks of economic disruption in the United States will mean a temporary halt in production by some manufacturers and a dip in consumer confidence. The recovery will then be driven by the strong US economy, consumer spending, public investment and government relief packages. The result will be a 4.2 percentage point drop in GDP. With 12 weeks of disruption, recovery with positive growth rates will not occur before Q4 2020, production will see lengthy delays, layoffs will drive down consumer demand and asset and credit bubbles may burst. In this scenario GDP growth could dive by as much as 7.1 percentage points.

A double whammy

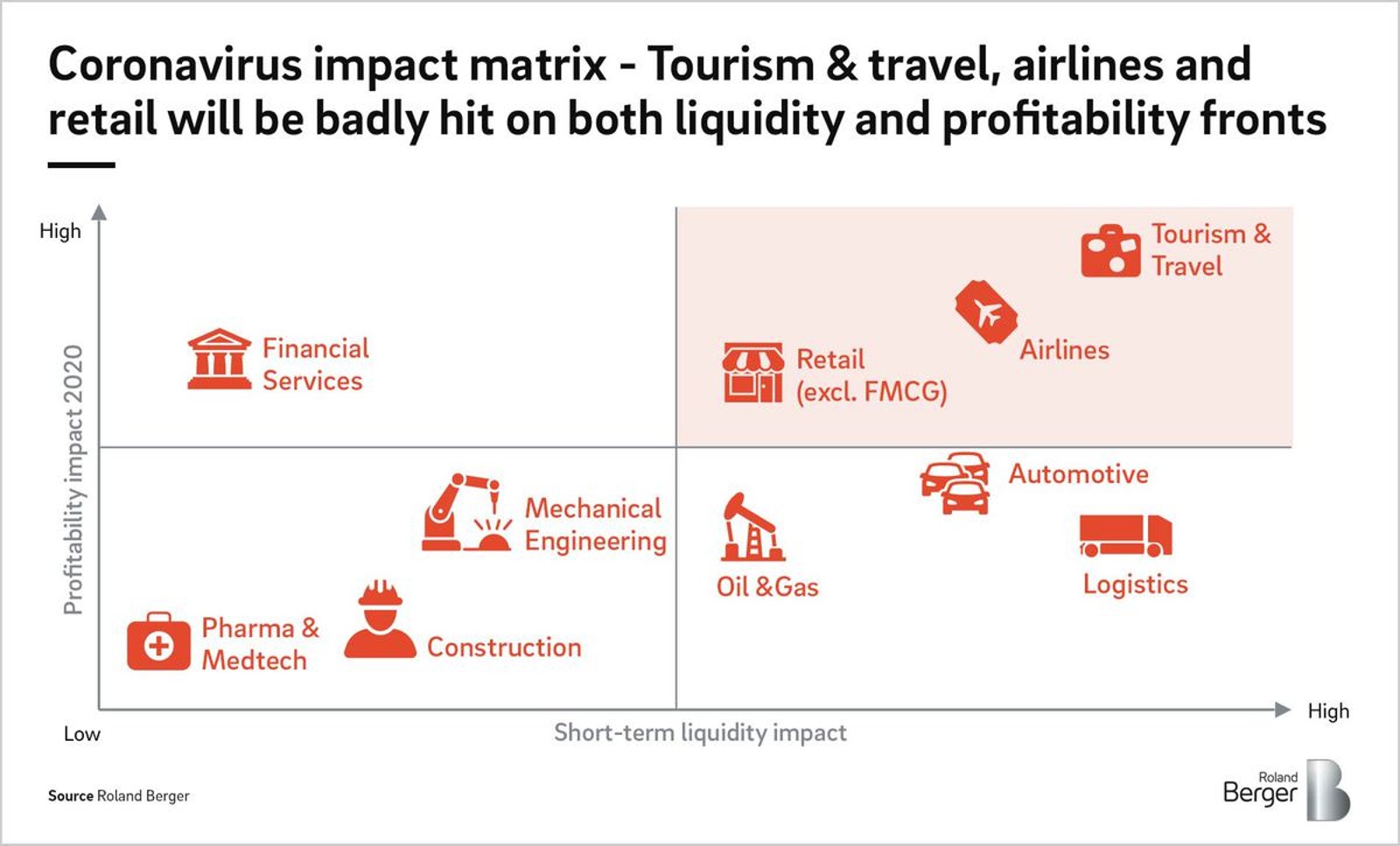

Whether the economic disruption lasts four weeks or twelve, the impact on industry will be two-fold, affecting both annual profitability and short-term liquidity. Tourism and travel, the airline industry and retail (excluding FMCG) will be hit strongly on both fronts, putting them in the upper right-hand quadrant of our coronavirus impact matrix below. Thus, tourism and travel have already experienced short-term cancellations and a sharp drop in cash inflow as new bookings for June to August evaporate. The industry has limited options for catching up after the crisis has ended, putting 2020 results under immense pressure. In the airline industry, last-minute cancellations combined with a tendency towards flexible bookings have led to a cash shortage; the long-term financing of aircraft limits the possibilities for adjusting cash outflow accordingly. Profitability will be impacted by the industry's close correlation with tourism and travel. Non-FMCG retail is seeing drastically reduced demand, leading to a shortfall in sales

The automotive, logistics and oil and gas industries will take a similar blow to short-term liquidity but demonstrate greater ability for their earnings to catch up after the crisis ends. In the automotive industry, demand will further drop off during the crisis, which will be particularly challenging for automotive suppliers with fixed cost structures. However, recovery in China may allow firms to make up for some of the losses they suffer. The logistics industry is seeing a big drop in profitability as production stops, but the rebound effects when the situation relaxes will allow for partial catch-up. The oil and gas industry has been through crises before and enjoys some flexibility due to third-party oilfield services. However, its liquidity situation is exacerbated by the current price war between Saudi Arabia and Russia: With an oil price of 30 USD/bbl, upstream free cash flow is close to zero.

The financial services industry will be less impacted in terms of short-term liquidity, but 2020 results will come under pressure. Low interest rates and monetary policy measures will provide financial aid during the crisis, although the inevitable bankruptcies will lead to reduced cash inflows for the industry. Profitability for the year will be affected strongly by the depreciation of distressed and bankrupt corporate financing, while regulatory requirements on core capital may lead to fire sales of credit portfolios.

These are our forecasts for industry if the economic disruption lasts four to twelve weeks. However, it cannot be ruled out that the crisis will cause much deeper, structural damage to the economy. With this in mind we have revised our third "Profound Recession" scenario downwards, to reflect multiple insolvencies, skyrocketing unemployment and governments unable to stimulate economic growth. In this worst-case scenario our forecasts are now that GDP would grow just 0.3 percent in China in 2020, and shrink by 9.3 percent in Europe and 10.4 percent in the United States.

Roland Berger is monitoring the impact of the spread of COVID-19 on a daily basis. For our latest updates and a detailed assessment of the impact on your region or industry, please contact [email protected] .

Further reading