MRO operators face tough times. The commercial aircraft, military aircraft, military vehicle and railway sectors experienced 40-50% declines in 2020, driven by the coronavirus pandemic. In this article, we outline a path to recovery, focusing on efficiencies. Our Digital MRO Matrix allows companies to assess their current status, and outlines a sustainable approach to first improve operational maturity and then implement digital transformation.

The maintenance, repair and overhaul (MRO) industry keeps things moving. Whether it is planes in the air or trains running on time, it covers all actions that keep a fleet item in working condition.

Safety requirements are therefore stringent, and MRO in the commercial aviation, military and railway sectors is highly regulated. Engineers who maintain planes and trains must be licensed, for example, and, in the aeronautical industry, MRO requirements are defined by airworthiness authorities.

But after safety, the overarching goal of fleet operators is to maximize asset availability at minimum cost. In short, efficiency is king and MRO providers must run lean maintenance processes. Doing so makes good business sense – boosting efficiency only helps to improve profitability.

Unfortunately, MRO companies are currently in need of some maintenance, repair and overhaul themselves. As a result of the coronavirus crisis and other market headwinds, players in the four key sectors of commercial aircraft, military aviation, military vehicle and rail are suffering immense cost and efficiency pressures.

We believe these challenges, outlined in more detail below, demand a fresh approach by the industry. In this report, we propose a matrix-based approach, focusing on two core elements of efficiency improvements:

improving operational process

maturity and strengthening digital maturity. First, we show how our Digital MRO Matrix and assessment tool can measure these maturity levels, including looking at current performance across the four MRO sectors. Then we outline how companies can improve maturity levels to boost efficiency and profits, giving use case examples. We find that to overcome the challenges facing them, MRO players need to improve their operational maturity before tackling digitalization maturity.

1. Tough times: The challenges facing MRO companies

Market situation

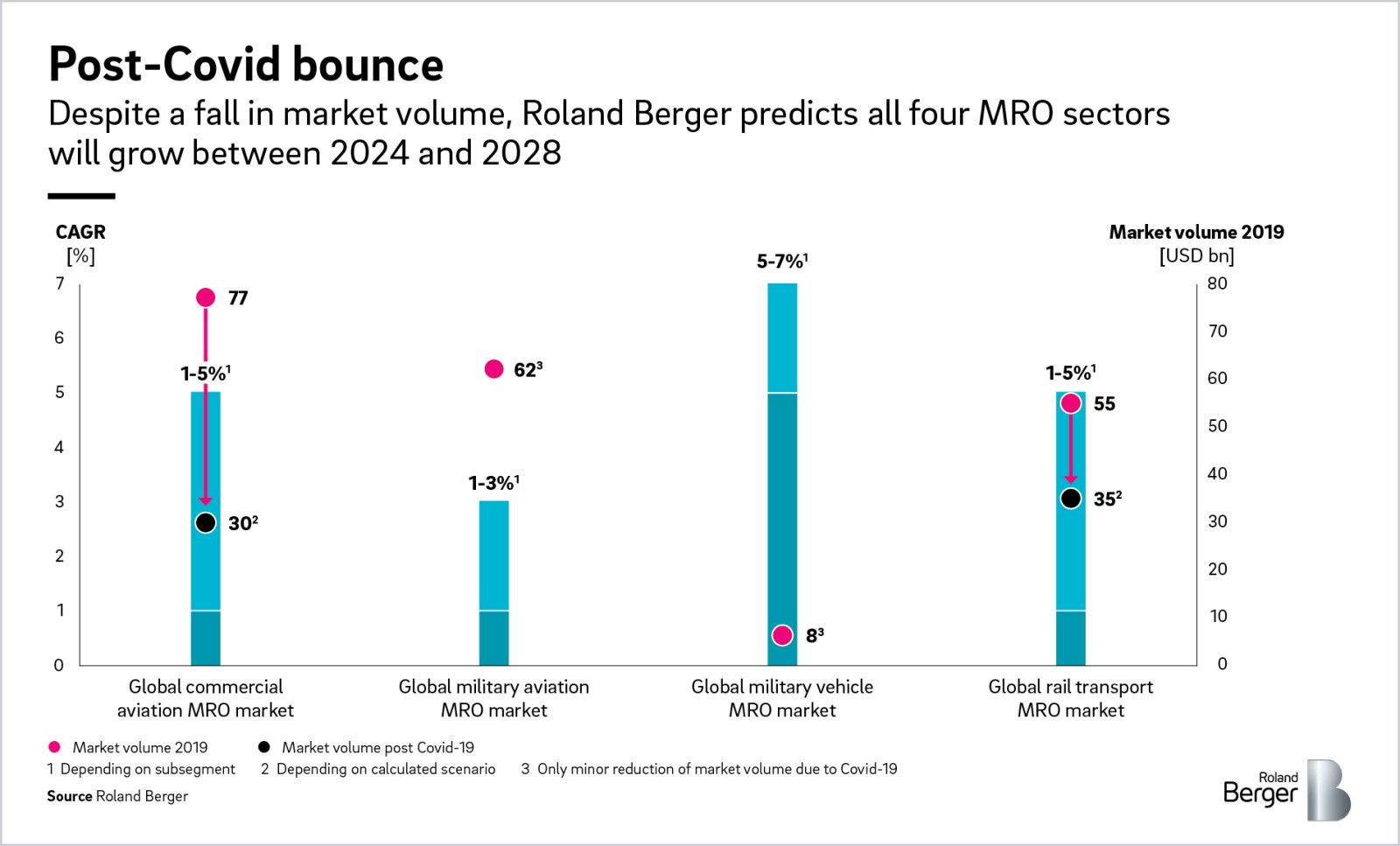

Before the coronavirus crisis, the global MRO market was strong and growing. Now it is in unprecedented decline. Roland Berger predicts that the crisis will halve market volume in the commercial aircraft MRO sector, with levels falling from nearly USD 80 billion in 2019 to an expected USD 30 billion once the ‘new normal’ is reached around 2024 – depending on the region. The rail transport sector will suffer falls of around 40%, while the military aviation and vehicle MRO market will see minor reductions.

We believe all four sectors will begin to recover once the new normal is reached, with annual growth of between 1% and 7% until 2025, albeit from a far lower base than before the crisis. The armored vehicle MRO market is expected to achieve the highest CAGR, at between 5% and 7%, due to the relatively low

impact of Covid-19

on this sector.

Market challenges

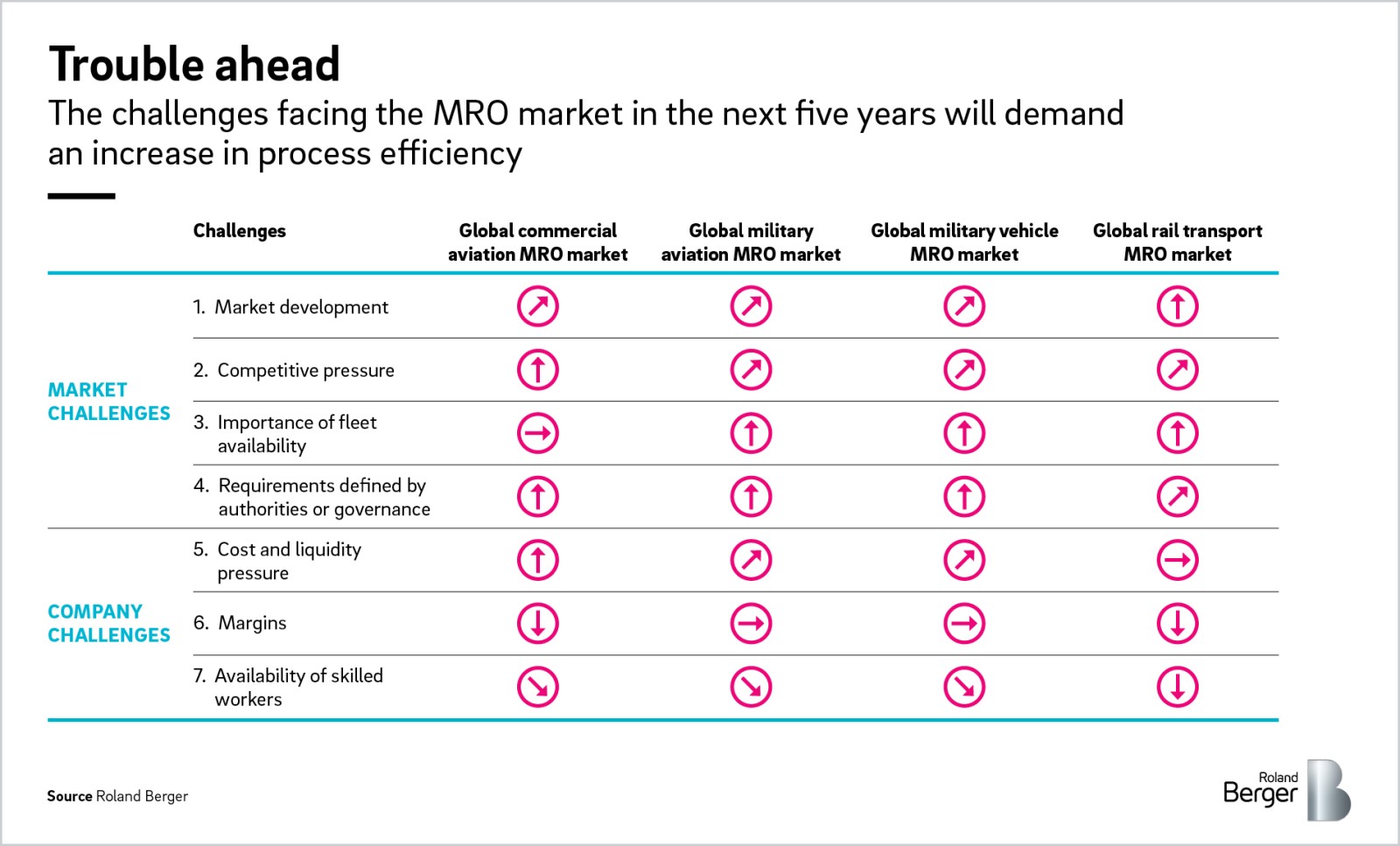

Besides the dramatic decline in volumes, several other headwinds are buffeting the MRO industry:

The next five years will be dominated by the impact of the coronavirus crisis. Commercial aviation MRO will feel the worst short-term effects as postponed activities lead to under-utilization. But in the medium to long term, companies in the sector can profit as airlines opt to extend the lifetimes of older aircraft to save money. Such a move will hit pre-Covid CO2 emissions targets, however.

The rail MRO sector is likely to grow over the next decade, driven by tougher emissions regulation and the public’s desire to lower its carbon footprint. Growing demand will require bigger fleets and therefore more MRO work.

The military aviation and military vehicle MRO sectors are also expected to grow in the coming years, as demand from developing countries continues to increase.

Two factors are causing increasing competitive pressure across all sectors. First, internal competition between MRO providers is rising, and second, rail and aircraft OEMs are increasingly edging into the MRO market.

As a result of the coronavirus-driven market collapse, there will be a fleet overcapacity in the commercial aviation sector. But in the other three sectors, the importance of availability will strongly increase.

As mentioned above, rail MRO is set to benefit in the long term from emissions concerns as more people turn to rail travel, whereas commercial aviation will suffer.

Many experienced MRO employees are set to retire over the next few years. This will leave a skills gap and force companies to develop apprentices and hire new workers.

An expert overview of the effects of these challenges on each sector is given in the graphic below.

2. Targeted solution: Our matrix-based approach

To fully overcome the current shop-floor challenges facing MRO sectors, we believe companies need to focus on two core elements of efficiency improvement:

Improving operational process maturity (lean MRO principles)

Strengthening the level of digitalization maturity

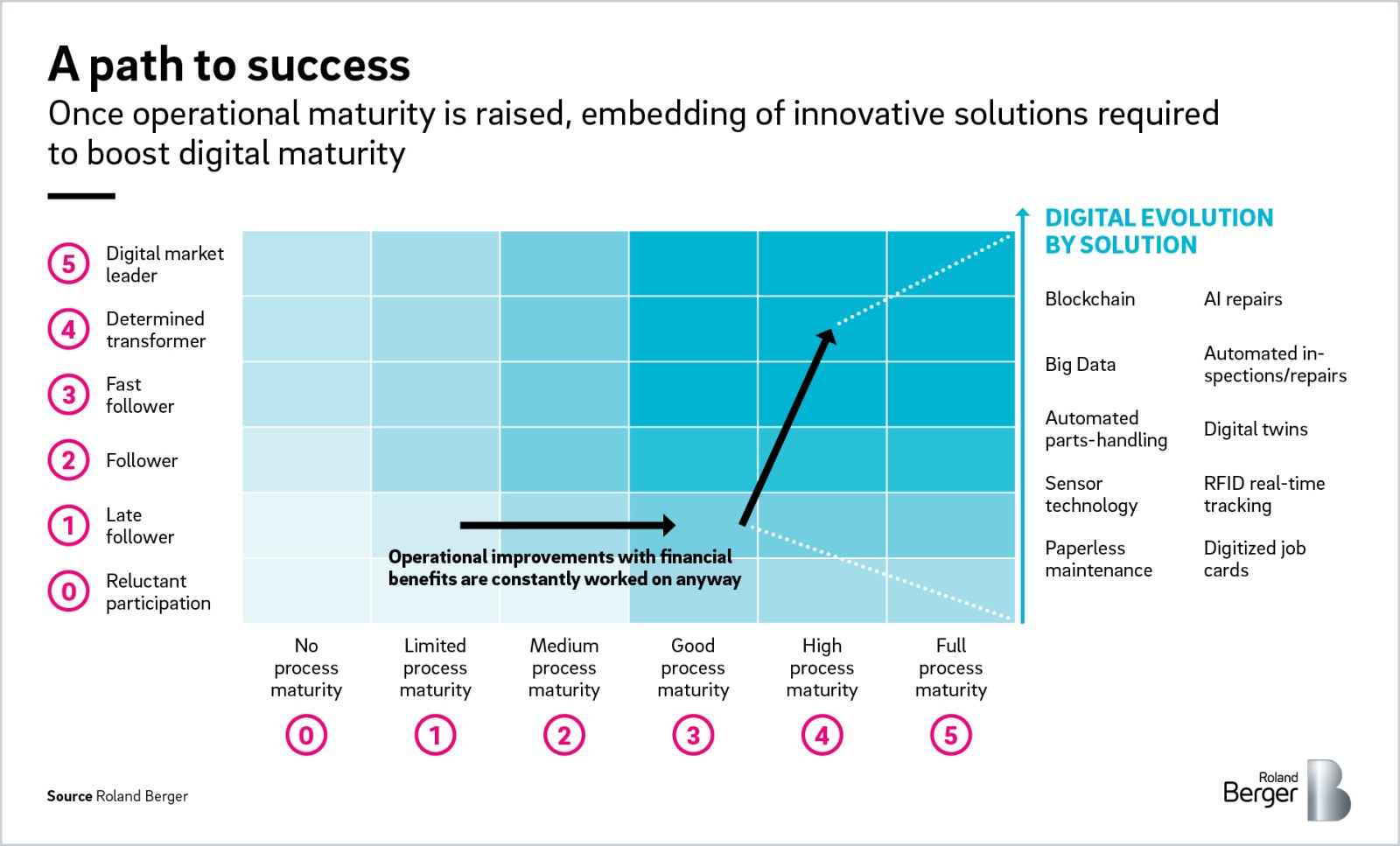

Assessing, understanding and improving these maturity levels is key to the success of MRO players. To help them, Roland Berger developed the Digital MRO Matrix (DMM). It separately plots levels of process maturity and digitalization maturity on a scale of 0 to 5, where a score of 5 in both means a fully digital and waste-free MRO operation.

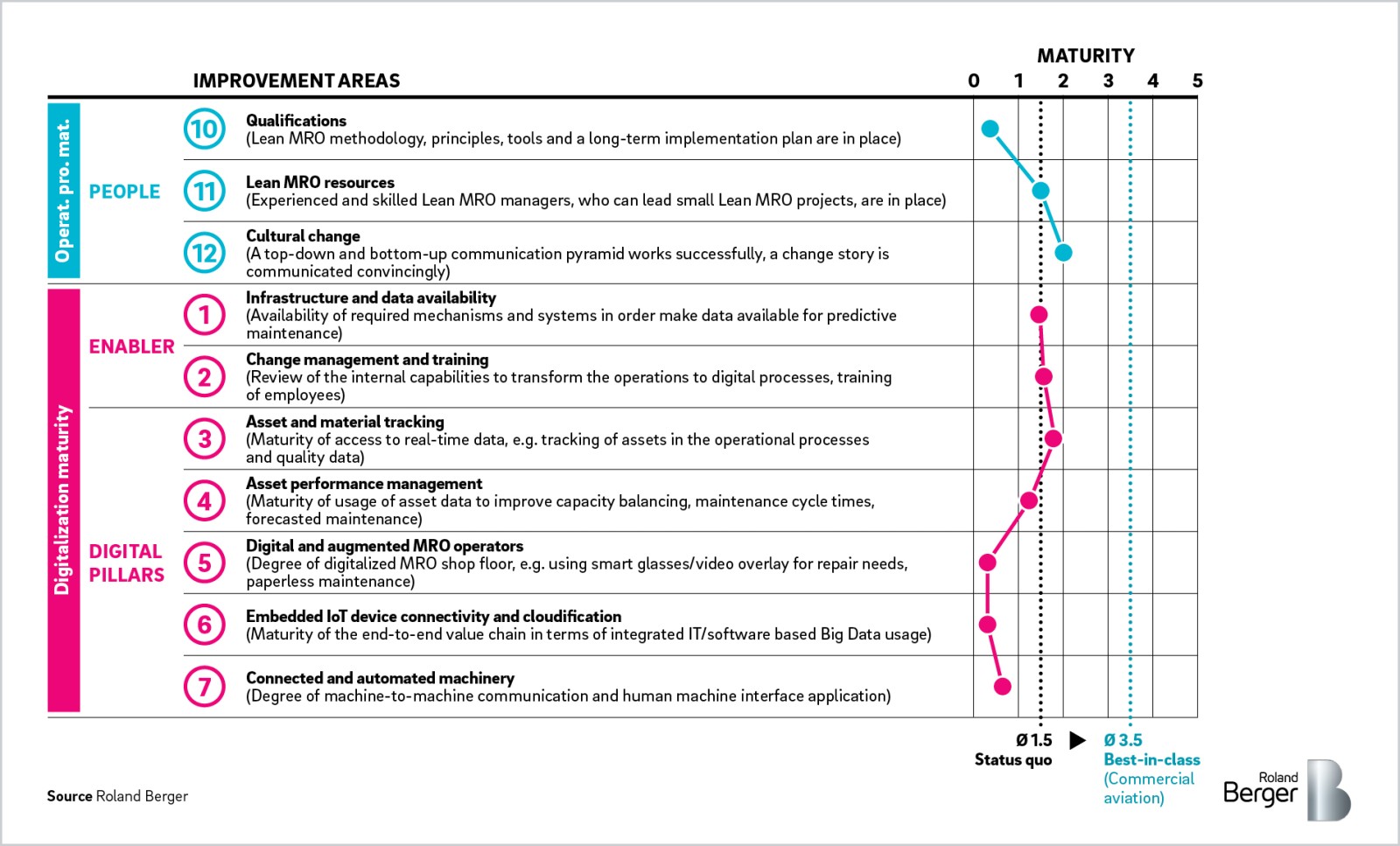

To determine levels of operational process and digitalization maturity, Roland Berger created the MRO assessment tool. It has been applied and proven among clients in the MRO industry, and we have also used it to measure the levels of the four key sectors themselves (see next chapter).

How it works

The first part of the tool focuses on the operational process assessment. It is clustered into 12 improvement areas, for example capacity planning and materials, with the maturity level of each determined by a comprehensive questionnaire. The second part assesses digitalization maturity. It determines maturity based on the availability and capability of basic enabling elements, such as infrastructure and training, and the presence or not of several key digital prerequisites, or pillars, such as advanced automation and artificial intelligence.

The graphic below provides more detail on the improvement areas as well as the maturity level of the best-in-class and worst-in-class industry performers. The dots indicate a typical company’s performance.

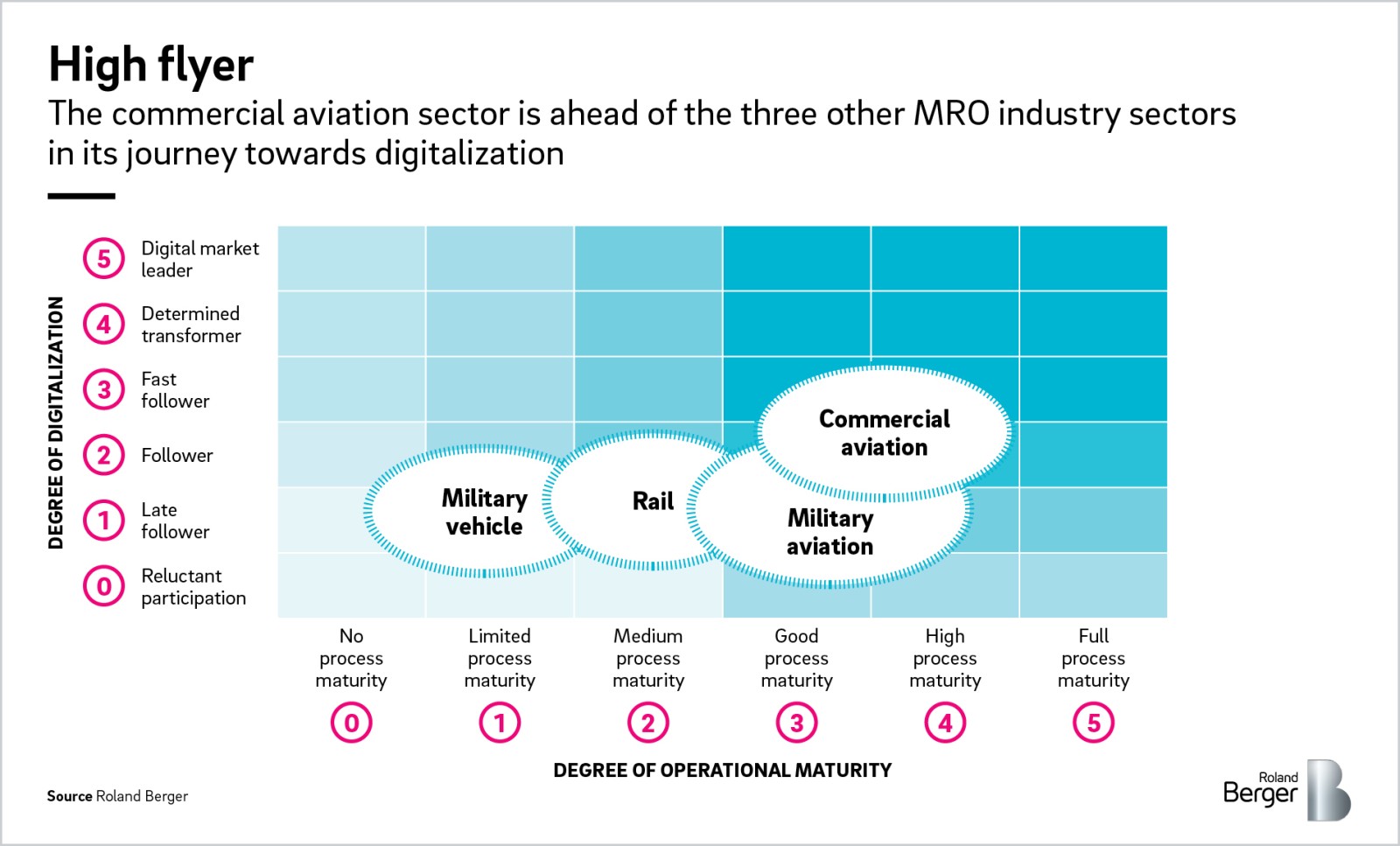

3. DMM results: Commercial aviation far out in front

Application of the assessment tool on the four key sectors of the MRO market provides an overview of the current industry landscape. The results show that the sectors are spread widely along the operational process scale of the DMM, but are all bunched around the late follower or follower level on the digitalization scale.

Commercial aviation

According to the DMM, the commercial

aviation industry

is the most advanced MRO sector. The sector’s high degree of process maturity is attributable to its overall quality culture, regulatory requirements and social awareness (zero-defect culture). But it still fails to reach a satisfactory level of digitalization. It achieves a higher score than the other sectors mainly because some single use cases, such as AI-driven predictive maintenance solutions, are in operation.

Military aviation

The defense aviation sector benefits from the same zero-defect culture as commercial aviation in terms of process maturity. However, regulation and sclerotic organizational structures currently limit further development. Asset availability also hinders process maturity. This lack of operational measures means military organizations currently have little focus on investment-intensive digital solutions.

Rail

With a medium process maturity and a follower status in terms of digitalization, rail companies still need to strengthen their process understanding and find an effective way to gather and track their heavy asset data. Some digital MRO solutions have been developed, but are still rarely used and suffer from operational process complications. These include AI-based identification of spare parts, or planning of cleaning activities based on visual AI-based scanning of graffiti-sprayed trains.

Military vehicle

The sector has the lowest level of digitalization and operational maturity. This is due to slow-moving, government-led internal processes that prevent operational-process improvements. Demand for asset availability also hinders development. As with military aviation, the sector needs to overcome fundamental changes to processes before pushing ahead with digitalization.

4. Improving process maturity: How to ease common pain points

Our assessment tool identified three improvement areas as major pain points that hold back the development of operational process maturity at MRO companies. In this chapter we outline these hurdles and propose recommendations to overcome them.

Daily shop-floor management

Strong leadership on the shop floor is key to improving operational processes. But we found that discussions about performance are seen as unnecessary and unlikely to lead to action. In addition, line managers do not take on a mandating role, and KPI-defined measure are not properly tracked, meaning solutions are not implemented. To address this:

Include a short (10 minutes) dialogue on performance in one of the shop-floor meetings that take place every day at MRO companies

Define a standard agenda for the meetings, including KPI deviations, problems, performance of measures, capacity planning and other relevant topics

Include Gemba walks in shop-floor management. Managers on different levels should walk along the value chain and address non-value adding activities.

Materials and tools

A common problem at MRO companies is that the right amounts and quality of

materials and tools

fail to arrive at the right location at the right time. To address this:

Stack appropriate tools and small consumables on trolleys

Deliver spare parts to a material station at least once a day

Store expensive tools in an automatic management and storage system close to the maintenance area to ensure they are readily available and secure.

Qualifications

With a disproportionate number of experienced employees due to retire from the MRO industry in the next few years, companies are being forced to address a coming skills shortage. To address this:

Hire new skilled workers and expand apprenticeship schemes

Ensure faster qualification of exiting employees and enhance cross qualification. The latter increases staff motivation and allows them to work efficiently between product or department types

Implement effective career management process to improve employee retention

5. Improving digitalization maturity: The key focus areas

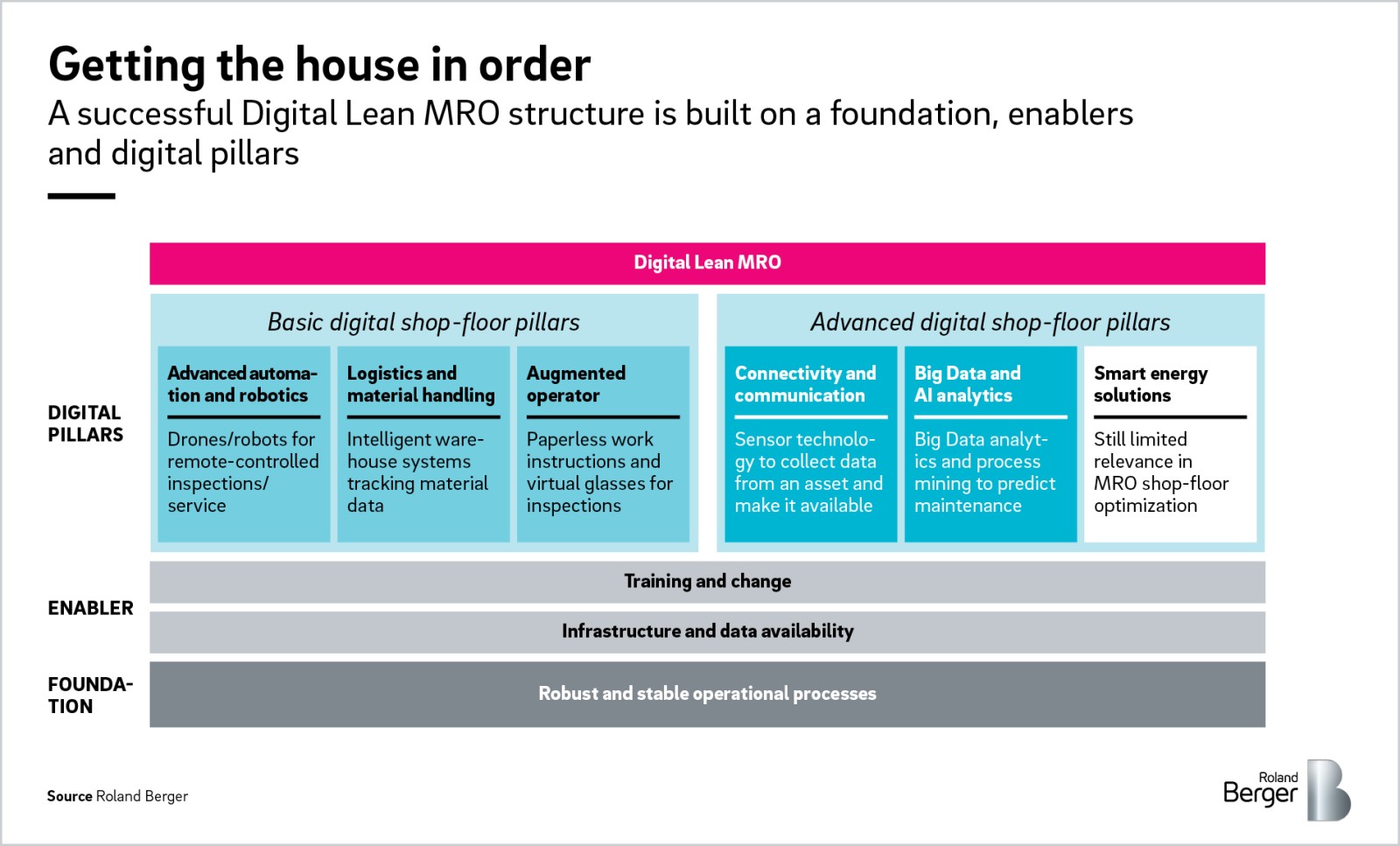

Before embarking on tailored digital solutions, we believe MRO operators should establish the fundamental foundation and enablers of digitalization. The foundation is a

robust

and stable level of operational process maturity. The enablers are twofold: 1) assets need to be equipped to collect data and maintenance software needs to be in place to synchronize it; and 2) the organization needs to be trained for, and capable of, executing the digital transformation.

Digital pillars

Once the foundations are in place, MRO operators need to focus on two key areas. First, put in place basic shop-floor digitalization improvements, then enact more advanced digitalization improvements.

The basic pillars focus on improving the operational processes enabled by digitalization. These are mainly catered MRO solutions, such as drone or robot-driven inspections, but also include non-MRO specific concepts like the installation of robot applications for part repairs, and initial systems to track parts. In addition, digital work plans and other digital documentation are key to improving workflows.

Advanced pillars relate to the sharing of available data, whereby it can be analyzed using defined algorithms. This enables end-to-end predictive maintenance. A top-end goal is being able to share information via cloud-based solutions along the entire value chain, including the intelligent steering of energy distribution.

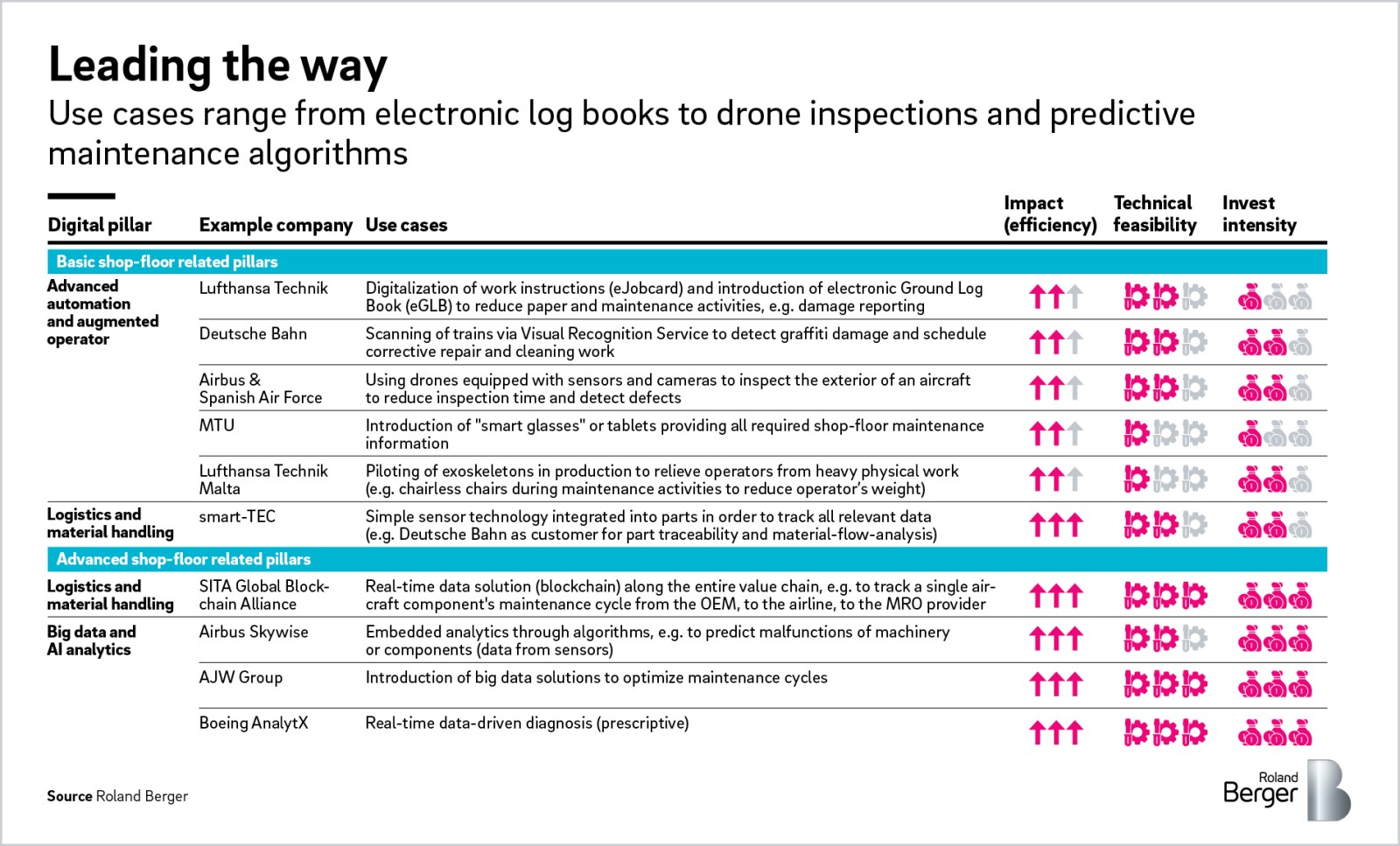

Use cases

The following table gives an overview of potential use cases for basic and advanced digital pillars, their impact, technical feasibility and investment needs, as well as providing examples of companies currently utilizing them.

Impact of digital pillars

These emerging technologies will have a considerable impact on efficiency. Combining digitalized basic shop-floor activities with end-to-end predictive solutions will, for example, result in average labor cost savings of 5-11% and turnaround time savings of 11-17%. Depending on their exact maintenance activities, some industries have a maximum potential of 15% and 27% respectively. The fall in spare part usage will also be significant, with an average inventory reduction of 10-20%, mainly realized through a more transparent logistics and material-handling process.

On top of efficiency savings, a further benefit of the pillars is safer installation and maintenance operations, potentially resulting in lower insurance costs, fewer work accidents and shorter down times.

Investment and implementation

Basic shop-floor initiatives, such as paperless maintenance or drone inspections, have low to medium investment requirements and a medium difficulty to implement. But when it comes to advanced pillars, we believe that MRO players still lack solutions to collect data (for example, sensor technology) and ensure that the correct data is available at the correct time. This are essential precursors to investment-intense end-to-end solutions, such as big data and the Internet of Things.

In summary, the industry landscape DMM in Chapter 4 displays a clear message for all MRO players around the globe: There is plenty of room for improvement! In the current market, service providers cannot afford to run inefficient operations. An efficient and digitalized shop floor using smart service solutions not only ensures considerable overall cost improvements, it also ensures competitiveness, and therefore survival. Robust and stable operational processes are a prerequisite of this.

To develop their operational processes and execute their digital transformation, players must first find their current position in the DMM. Roland Berger offers support in assessing a firm's MRO process maturity, can identify operational gaps and define a strategic roadmap to boost its operations and become a determined transformer.

Sign up for our newsletter

Register now to receive regular insights into our Operations topics.